Hand-crafted by Flo, auto-checked by AI.

Resources

Product and Service Costing takes the costs incurred in cost-type and cost-center accounting and assigns them to the products or services that caused them. This is often done using cost drivers, which are factors that influence the level of costs. This answers the question: For which products or services have the costs been incurred?

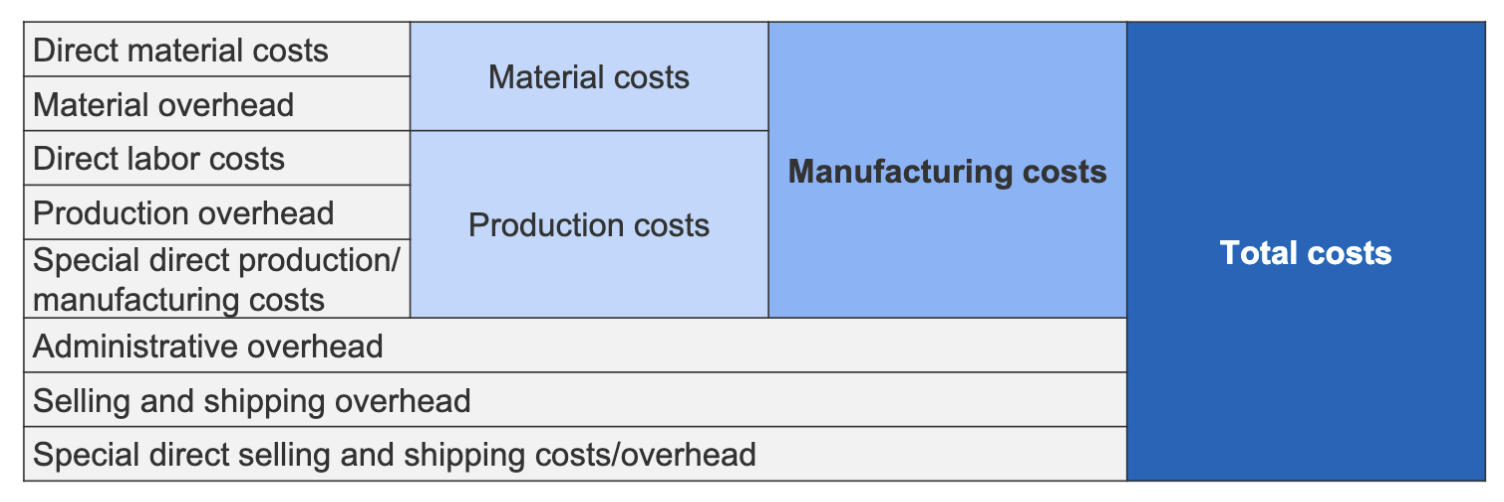

It serves planning (production decisions, sales prices), control (cost and performance) and documentation (inventory valuation) purposes. Results are split into manufacturing costs (direct materials, direct labor, manufacturing) and total costs (manufacturing + r&d + selling and administrative costs). The latter is relevant for pricing decisions, while the former is relevant for inventory valuation and cost control.

Classifying Cost Objects

Cost objects are classified in 4 dimensions to assign costs to them:

- Production Stage: Final or intermediate product

- Purpose: External (to be sold) or internal (used by the company)

- Production Relation: Non-connected products or joint (e.g. hydrogen and oxygen) and by-products

- Type of Goods: Tangible or intangible goods

Costing for Low Quantities

Individual production (tankers, large-scale plants, tailor-made clothing, films) and batch production (business cards, car models, wine) use job costing or machine hour costing, which assign costs based on the specific jobs or machine hours used for each product. Costs may vary significantly between different products and production runs.

Job Costing

In job costing, costs are divided into:

- Direct costs: directly traceable to a specific job (e.g. materials, labor).

- Indirect costs: not directly traceable to a specific job, but allocated based on a cost driver (e.g. machine hours, labor hours).

Single Rates

Single rates allocate all indirect costs using a single cost driver, such as machine hours or labor hours. This is simple but may not accurately reflect the true cost of different jobs.

Volume-Based Rate

Indirect costs can be assigned to a job using a volume-based rate like the hourly production rate (in €/h) derived from annual costs and hours, which is then multiplied by the hours spent on the job to allocate overhead costs.

Value-Based Rate

Another method are value-based overhead rates (in %), which derives from the the relationship between a set of direct and overhead costs, and is applied to the direct costs of a job to allocate overhead costs.

This allocates more overhead to more expensive products with the same production time, which can represent reality more accurately, but may also distort costs for low-volume products.

Multiple Rates

Breaking down overhead costs by cost center and using different cost drivers for each center can provide a more accurate allocation of costs. For example, machine-related costs may be allocated based on machine hours, while labor-related costs may be allocated based on labor hours. This method is more complex to implement but can lead to better cost control and pricing decisions.

| Cost center | Allocation base | Overhead rate or cost rate |

|---|---|---|

| Material | • Quantity of material consumed • Direct material | • Cost rate per unit • Overhead rate on material costs |

| Manufacturing | • Machine hours • Production hours • Quantity of output • Direct labor | • Cost rate per hour • Cost rate per unit • Overhead rate on production wages |

| Administration | • Hours of administrative work • Quantity of administrative services • Direct labor • Manufacturing costs | • Cost rate per hour • Cost rate per unit • Overhead rate on direct labor • Overhead rate on manufacturing costs |

| Selling and shipping | • Direct labor • Manufacturing costs | • Overhead rate on direct labor • Overhead rate on manufacturing costs |

Manufacturing and SGA

In many companies, costs are split into manufacturing costs (direct and overhead materials, direct labor and production overhead) and selling, general, and administrative (S,G&A) costs.

For cost allocation purposes, manufacturing costs are typically allocated to products based on production-related cost drivers, while SGA costs may be allocated based on sales or other relevant drivers.

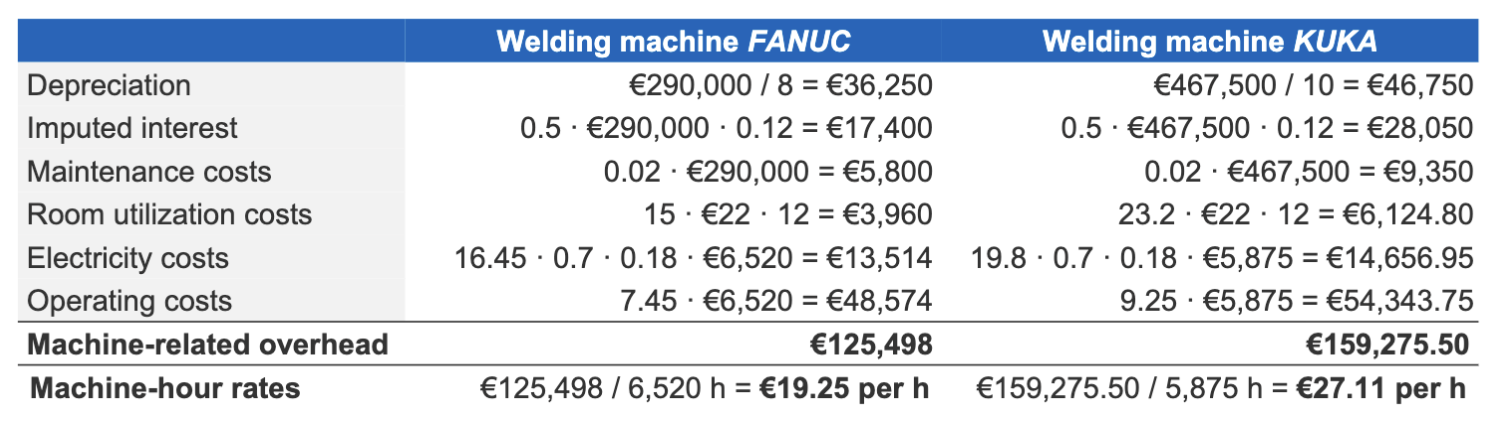

Machine Hours

Due to the increasing automation of production processes and computer-enabled flexible manfucturing systems, machine hours have become a relevant cost driver in comparison to labor cost or production time. Machine-hour costing is a specific form of job costing that breaks down machine-related overhead by machine and allocation.

Determining the machine-hour cost rate includes the yearly depreciation and imputed interest, as well as maintenance, room, electricity, and operating costs, which is then divided by the yearly machine hours available.

Time of Job Costing

Job costing occurs at three different times: normal/preliminary costing happens before production, which is used for planning and pricing decisions; interim costing happens right after job completion and is used for cost control and performance evaluation; and actual/post costing happens after inventory valuation and is used for documentation purposes.

- Preliminary Costing: Uses planned direct and overhead costs to determine the total planned costs

- Interim Costing: Uses actual direct costs and normal overhead costs (as these are only allocated at the end of the year) to determine the total interim costs

- Actual Costing: Uses average actual direct and overhead costs to determine the total actual costs

Normal overhead costs are the average of the past few years and the actual cost-allocation base.

Bookkeeping

Manufacturing costs flow through the accounting system as they move through the production process:

- Work in Progress (WIP): Costs are accumulated as production begins (direct material from raw material; direct labor from wages for jobs; overhead allovated using predetermined or normal rates).

- Finished Goods: Upon job completion, total manufacturing costs are transferred from WIP to Finished Goods inventory.

- Cost of Goods Sold (COGS): When the product is sold, costs move from Finished Goods to the COGS account.

Costing for High Quantities

Variant production (magazines, chemicals, microprocessors) and mass production (electricity, cement, pencils) use process costing or the equivalence number method, which assign costs based on the average cost per unit of production. Costs are more uniform across products and production runs.

Single-Stage Process Costing

In single-stage process costing, costs are accumulated for the entire process, and then allocated to products based on the quantity produced. This method is suitable for industries where products are homogeneous and go through a single production process (water, forestry, electricity).

Multi-Stage Process Costing

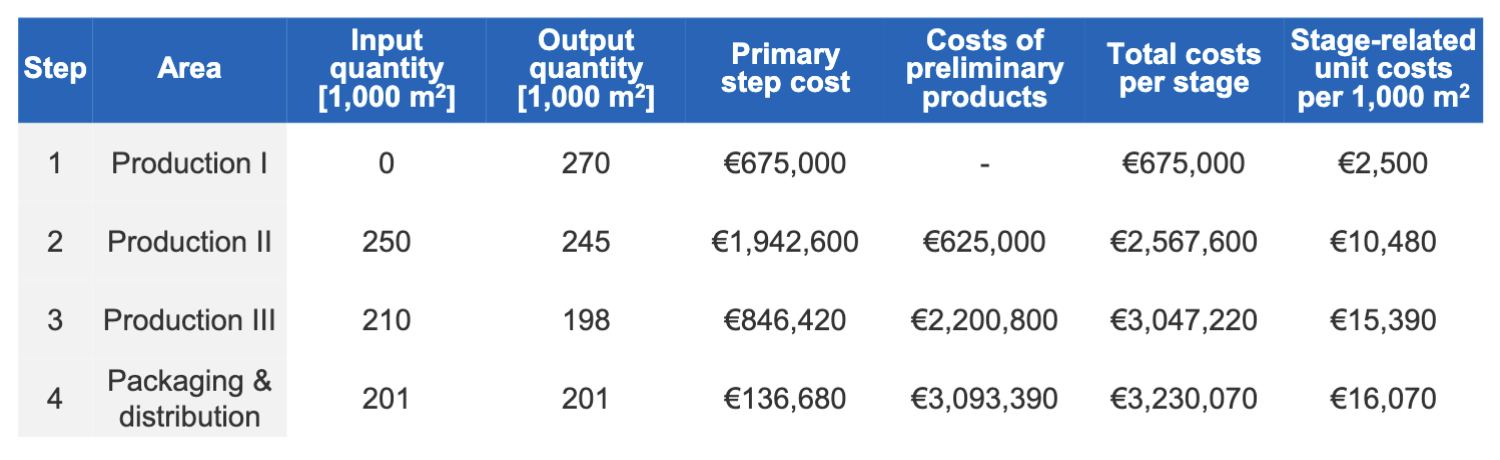

When products go through multiple stages of production (e.g. different quality standards, varying stock changes), costs are accumulated for each stage and allocated to products based on the quantity produced at each stage. This method is suitable for industries where products are heterogeneous and go through multiple production processes (chemicals, microprocessors), however requires tracking costs at a department level.

To identify the stage-related unit costs, the primary costs of the stage are added to the aggregated costs from the previous stage (previous stage-related costs multiplied by current input quantity) and divided by the current output quantity. The stage-related unit costs of the final stage are the total unit costs of the product, which can be used for pricing decisions and inventory valuation.

If production of a given stage is not yet completed, the number of equivalent units (finished and unfinished) is determined to find the cost per equivalent unit. Finished products receive the full cost per unit, while unfinished products receive a proportion of the cost based on their stage of completion.

Equivalence Number Method

The equivalence number method is used when products are heterogeneous but go through the same production process (e.g. different types of drink). Each product is assigned an equivalence number based on its relative cost compared to a base product. Costs are then allocated based on the equivalence numbers, which allows for a more accurate allocation of costs to different products.

Joint and By-Products

When multiple products are produced from the same process, there are three approaches to allocate costs.

Main-Product Method

Products are broken down into main products and by-products, and all costs are allocated to the main product. Profits of by-products are deducted from the main product’s cost.

Distribution Method: Volume and Value

Costs incurred before the decoupling point (where products become distinguishable) are allocated to each product based on either their production volume (quantity or weight) or their market values minus direct costs for the product. Profit is then determined for all products individually.

Inventory Value

For intangible goods, there is no change in inventory value. For tangible goods (e.g. unfinished products), the change is simply calculated as:

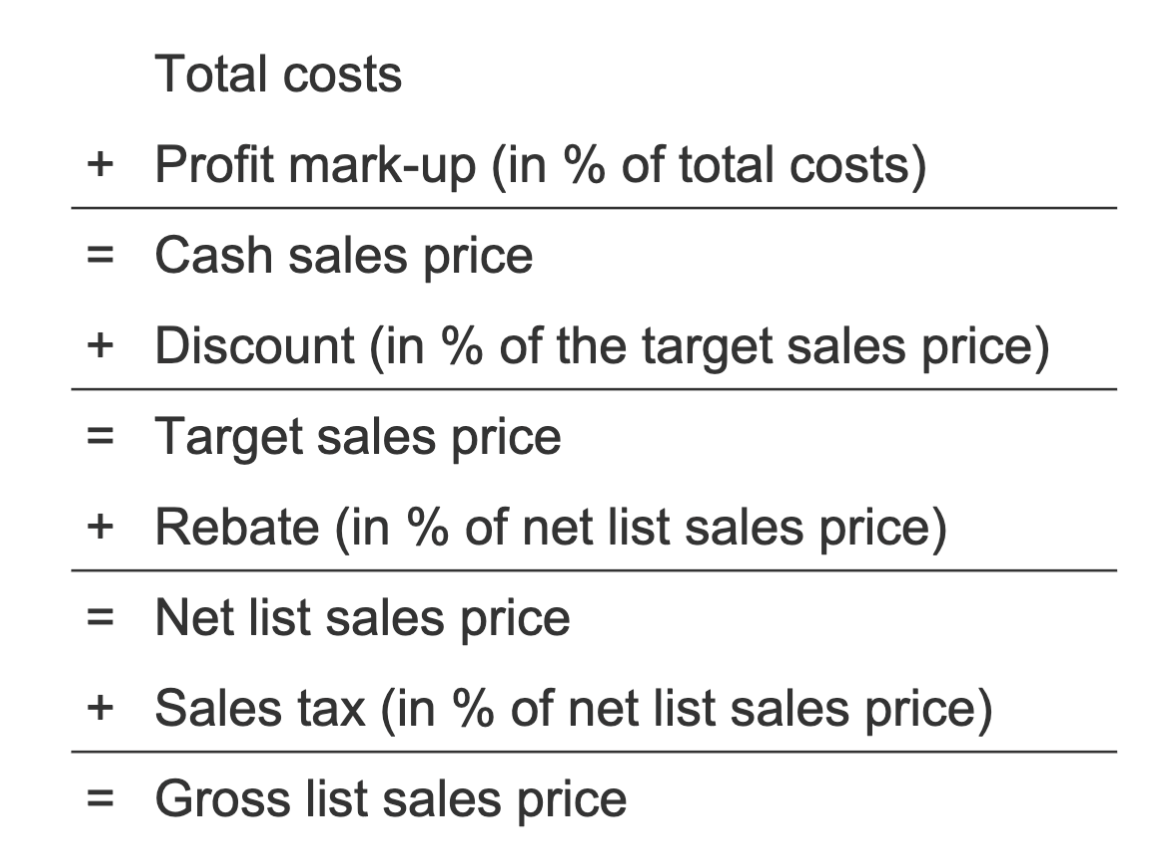

Sales Cost Makeup