Resources

Similar to cost types, centers, objects; profit and loss calculation considers revenue objects that can be based on revenue types and centers. A cost center combined with a revenue center is called a profit center, which determines the profit of one section of the company.

Costs and revenues can be linked for private companies generating revenues (not e.g. social organizations, for which other indicators have to be found). To find the profit per unit, unit costs and prices have to be determined. For the net profit of a period, the total costs and revenues of the period can be used.

Preparing an Income Statement

Typically, a companies production and sales volumes in a period are not the same, therefore typical revenues and costs for the actual production and sales volumes have to be determined. The nature of expense approach uses the quantity produced as cost basis, whereas the cost of sales approach uses the quantity sold as cost basis.

Income Statements in Financial Accounting and Cost Accounting

Valuating inventory is relevant for income statements financial accounting just like it is for cost accounting. Companies reporting in accordance with HGB frequently choose the nature of expense method, whereas IFRS reporting often uses the cost of sales method. However, in financial accounting measuring finished and unfinished inventory is regulated, while in cost accounting it isn’t.

Vertical Form and Account Form

The vertical form of an income statement lists revenues and expenses in a single column, while the account form presents them in two separate columns (debit and credit). The choice between these formats can depend on the company’s reporting preferences and the complexity of its operations.

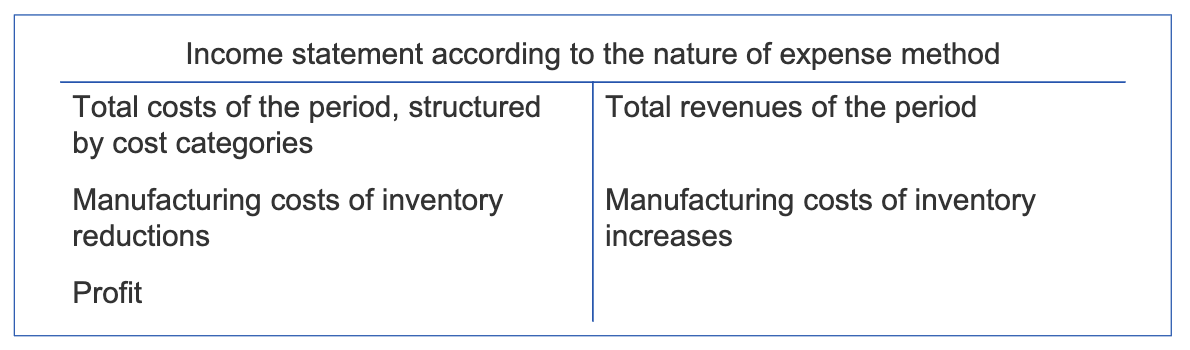

Nature of Expense Approach

This method compares the total costs of all produced products with the total revenues of all sold products of a period. Deviations between produced and sold quantities are taken into account as inventory changes. The profit is therefore the difference between revenues + manufacturing costs of inventory increase and the negative total costs minus the manufacturing costs of inventory reductions:

The structure of the income statement therefore adds inventory reductions on the debit side, and inventory increases on the credit side:

The nature of expense method is simple to calculate and integrates well with double-entry bookkeeping. It provides an overview of cost type structures, highlights inventory changes, and cost categories are usually already determined. It’s therefore commonly used in smaller enterprises.

However, it requires inventory recording (including value changes and unit cost calculations), doesn’t provide profit on product or functional area level and does not differentiate different cost structures between departments.

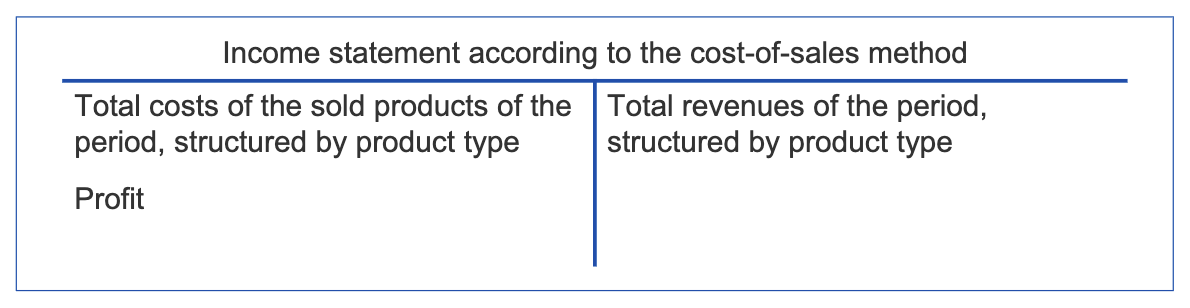

Cost of Sales Approach

This method directly compares costs and revenues on a product level. This requires performing product costing (determining the unit cost, including admin, sales, shipping). The cost of a period is given by the quantity sold, times a products unit cost. The profit is then simply the difference between revenues and cost of sales:

The cost of sales approach does not require stocktaking, is very fast and enables profit analysis on a product level. However, it’s not well integrated with double-entry bookkeeping and requires a calculation of total costs based on unit costs, which can be difficult to determine. It’s therefore more commonly used in larger enterprises and internationally, though there is a trend towards it for SMEs as well

Absorption and Variable Costing

In absorption costing, all manufacturing costs are allocated to products, including fixed manufacturing overhead. In variable costing, only variable manufacturing costs are allocated to products, while fixed manufacturing overhead is treated as a period cost and expensed in the period incurred. This influences the value of the change in inventory. Since absorption costing includes fixed manufacturing overheads in the cost of inventory, it will lead to higher profits when inventory increases.

Impact on Profit

- Inventory stays the same: No impact on profit.

- Inventory increases: Absorption costing shows higher profit than variable costing.

- Inventory decreases: Absorption costing shows lower profit than variable costing.

Incentives

Since absorption costing allocates fixed manufacturing overhead to products, it can create incentives for managers to overproduce in order to increase inventory and thus profit. Variable costing does not create this incentive. To combat this, companies may consider imputed interest costs on inventory, limited storage capacity, control of production and inventory volumes, multi-year income compensation systems, or linking bonuses to reaching or falling below inventory levels.

Contribution Margin Accounting

The contribution margin is the difference between revenues and variable costs. It represents the amount available to cover fixed costs and contribute to profit. Contribution margin accounting focuses on analyzing the contribution margin to make decisions about pricing, product mix, and cost control. Contribution margin accounting is an extended cost-of-sales method under variable costing in vertical form and a special income statement format and can be based on:

- Simple contribution margin: Summary and allocation of all fixed costs in one block.

- Multi-leveled contribution margin: Allocation of fixed costs on product, group, divisional, and company level.

This is relevant as absorption costing might indicate a loss on a product, even though its contribution margin is positive.