Resources

The accounting system is based on 3 pillars: Financial Accounting, Capital Budgeting, and Management Accounting. Management accounting broadly includes non-financial information as well as monetary information - cost accounting.

Management accounting is highly customized for each company, according to information requirements and often focusing on specific parts of the company. However, some people question whether the overhead of maintaining two accounting systems is justified. A study found 60% of companies to use a management accounting system harmonized with financial accounting law (Engelen and Pelger, 2014).

The Role of Cost Accounting

Cost accounting in the context of management accounting provides 4 key functions:

- Control: Identifying and managing costs to ensure they are within budget and the product suits the market.

- Monitoring: Tracking costs over time to identify trends, variances, and areas for improvement.

- Planning: Using cost information to plan future activities, set budgets, and make strategic decisions.

- Documentation: Keeping detailed records of costs for analysis, reporting, and decision-making.

Differences to Financial Accounting

Management accounting addresses planning, management, control and decision making for internal purposes, versus the presentation of financial information to external stakeholders. It’s hardly subject to rules and builds on disaggregated accounts across the company. It’s both future- and past-oriented and variable in time and frequency.

Differences to Capital Budgeting

Capital budgeting focuses on long-term investment decisions, evaluating the profitability and risks of potential projects. Cost accounting however neglects the time value of money and focuses on the costs associated with production and operations. It is more concerned with short-term cost management and control rather than long-term investment decisions.

Costs

Costs Definition

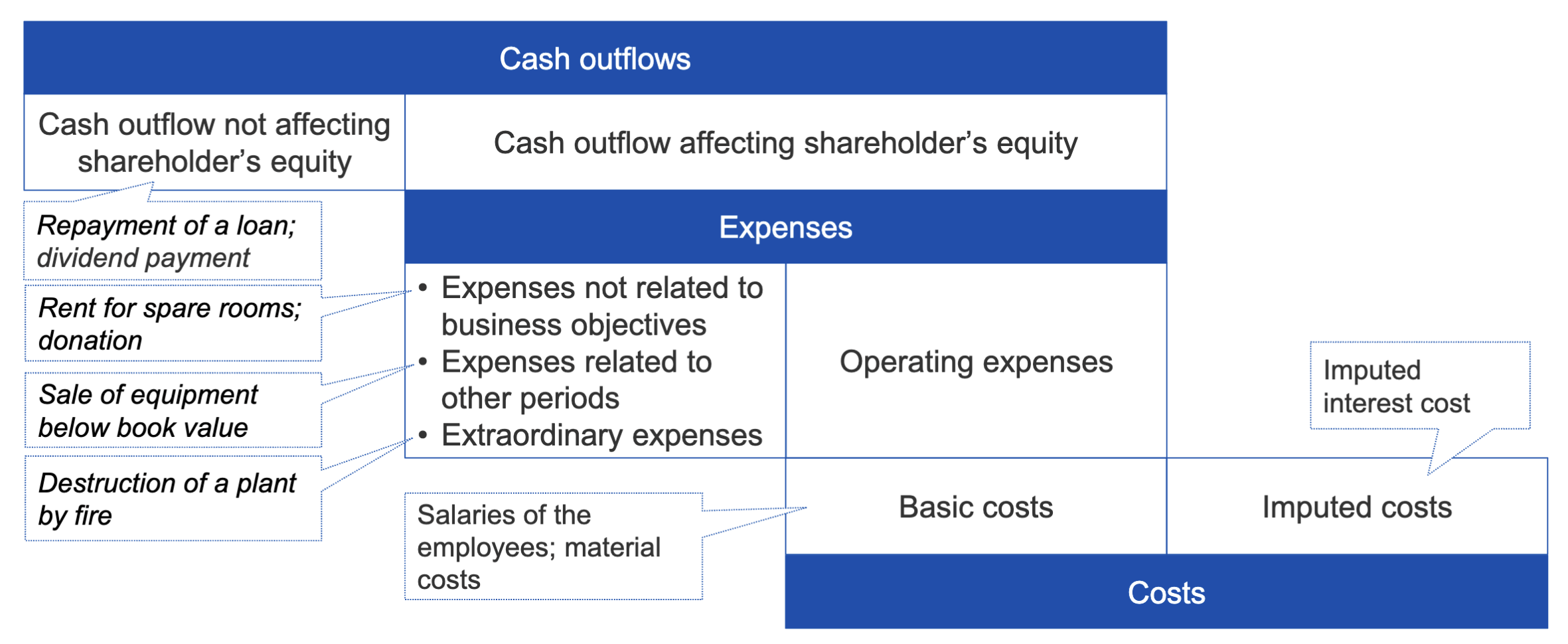

Costs are not cash flows. They are the monetary value of resources used in production or operations, regardless of when the cash flow occurs. Similarly, revenues represent the monetary value of goods or services sold, not necessarily when the cash is received.

Costs and revenues imply three major components:

- Objective Oriented: They are associated with a specific objective of the organization, such as a product, project, or department

- Monetary Value: They are expressed in monetary terms, representing the value of resources consumed or generated.

- Resource Usage: They reflect the consumption of resources, such as labor, materials, and overhead, in the production or delivery of goods and services.

Costs relate to Cost Accounting, while expenses are part of Financial Accounting. German companies often differentiate between the two, while many international companies use the terms for similar concepts.

Total Costs and Unit Costs

Total and unit costs help understand the overall cost structure of a product or service.

- Total Costs: All costs associated with all goods produced in a period, including fixed and variable costs. They represent the overall cost of production or operations for a specific period.

- Unit Costs: The cost per unit of output, calculated by dividing total costs by the number of units produced. They help in pricing decisions and cost control.

Because fixed costs are allocated over more units as production increases, average unit costs decrease with higher production volumes. Therefore, average unit costs (total costs divided by quantity) typically decrease with scale – known as economies of scale.

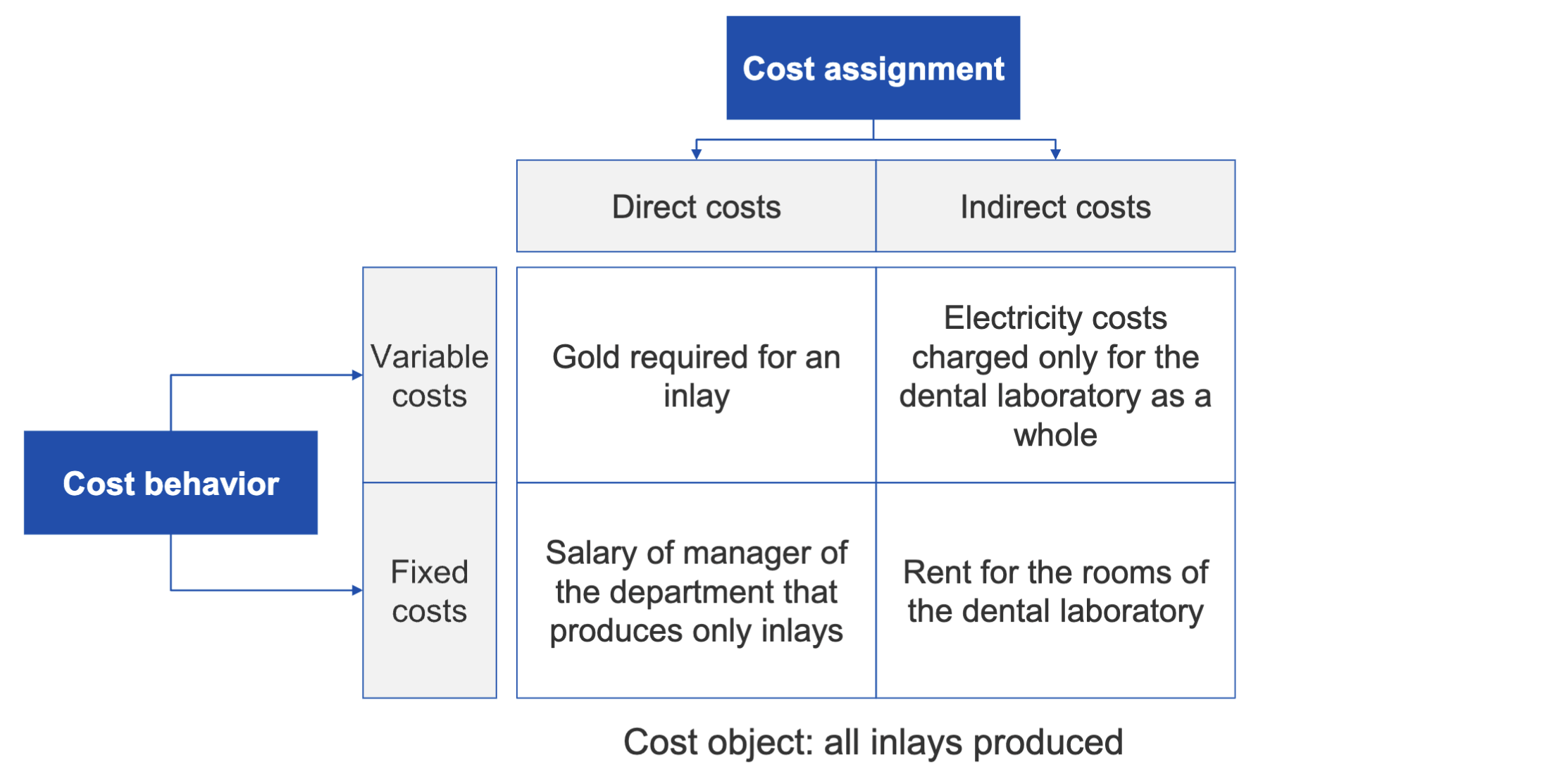

Direct and Indirect Costs

Direct and indirect costs are classified based on their traceability to a specific cost object.

- Direct Costs: Costs that can be directly traced to a specific cost object, such as raw materials or direct labor.

- Indirect Costs: Costs that cannot be directly traced to a specific cost object and are often allocated, such as overhead costs like rent or utilities.

- Artificial Indirect Costs: Costs that could be directly traced but are treated as indirect for simplicity, such as certain administrative expenses.

Variable and Fixed Costs

Variable and fixed costs are classified based on their behavior with changes in production volume.

- Variable Costs: Costs that change in direct proportion to the cost driver (production volume), such as raw materials and direct labor.

- Fixed Costs: Costs that remain constant regardless of the cost driver, such as rent and salaries of administrative staff.

There is typically a linear relationship between variable/fixed and total costs, starting at the fixed cost level and increasing with variable costs as production increases: .

Inventoriable and Periodic Costs

Inventoriable and periodic costs are classified based on their treatment in inventory and financial statements.

- Inventoriable Costs: Costs that are assigned to a specific product unit and included in inventory until the product is sold, at which point they become part of the cost of goods sold. They include direct materials, direct labor, and manufacturing overhead.

- Periodic Costs: Costs that cannot be capitalized and are expensed in the period they are incurred. They include selling, general, and administrative expenses.

Opportunity and Sunk Costs

Opportunity and sunk costs are classified based on their relevance to decision-making.

- Opportunity Costs: The potential benefit that is foregone by choosing one alternative over another. They represent the value of the next best alternative that is not chosen.

- Sunk Costs: Costs that have already been incurred and cannot be recovered. They should not influence future decision-making as they are irrelevant to current and future costs. For example, costs that have already been committed to a constructed power plant.

- Levelized Product Cost: The average cost per unit of output over the lifetime of a project, calculated by dividing the total costs by the total units produced. It is often used in capital budgeting to evaluate long-term projects. For example, the levelized cost of electricity (LCOE) to compare the cost-effectiveness of different energy generation technologies.

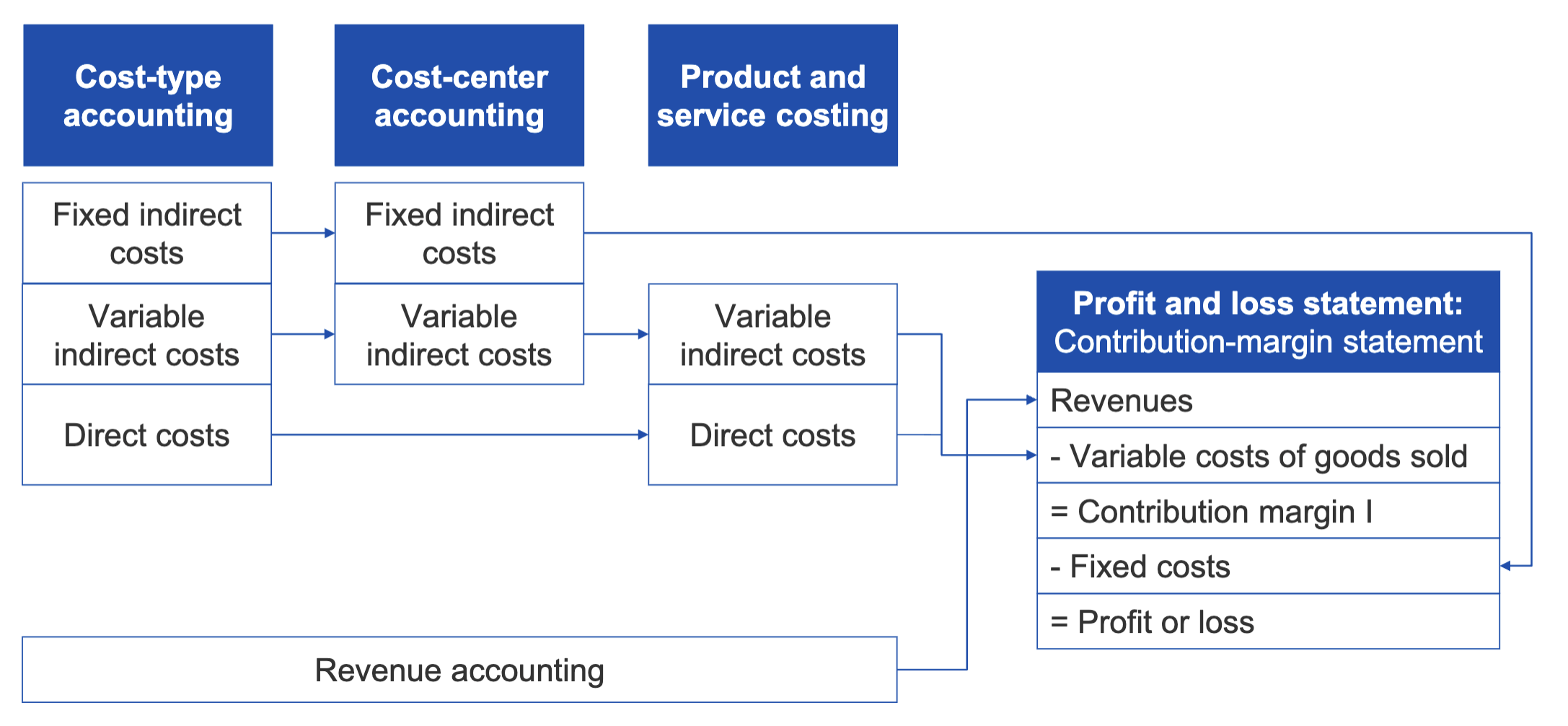

Absorption and Variable Costing

Absorption and variable costing are two methods of costing that differ in how they treat fixed manufacturing overhead costs.

- Absorption Costing: A costing method that includes all manufacturing costs (variable and fixed) in the cost of a product. It is required for external financial reporting under generally accepted accounting principles (GAAP).

- Variable Costing: A costing method that includes only variable manufacturing costs in the cost of a product. Fixed manufacturing overhead is treated as a period cost and expensed in the period incurred. It is often used for internal decision-making and management accounting purposes.

Contribution Margin: The contribution margin is the difference between sales revenue and variable costs. It represents the amount available to cover fixed costs and contribute to profit, even if the product is not profitable on an absorption costing basis. This should always be positive.

| Absorption Costing | Variable Costing |

|---|---|

|  |

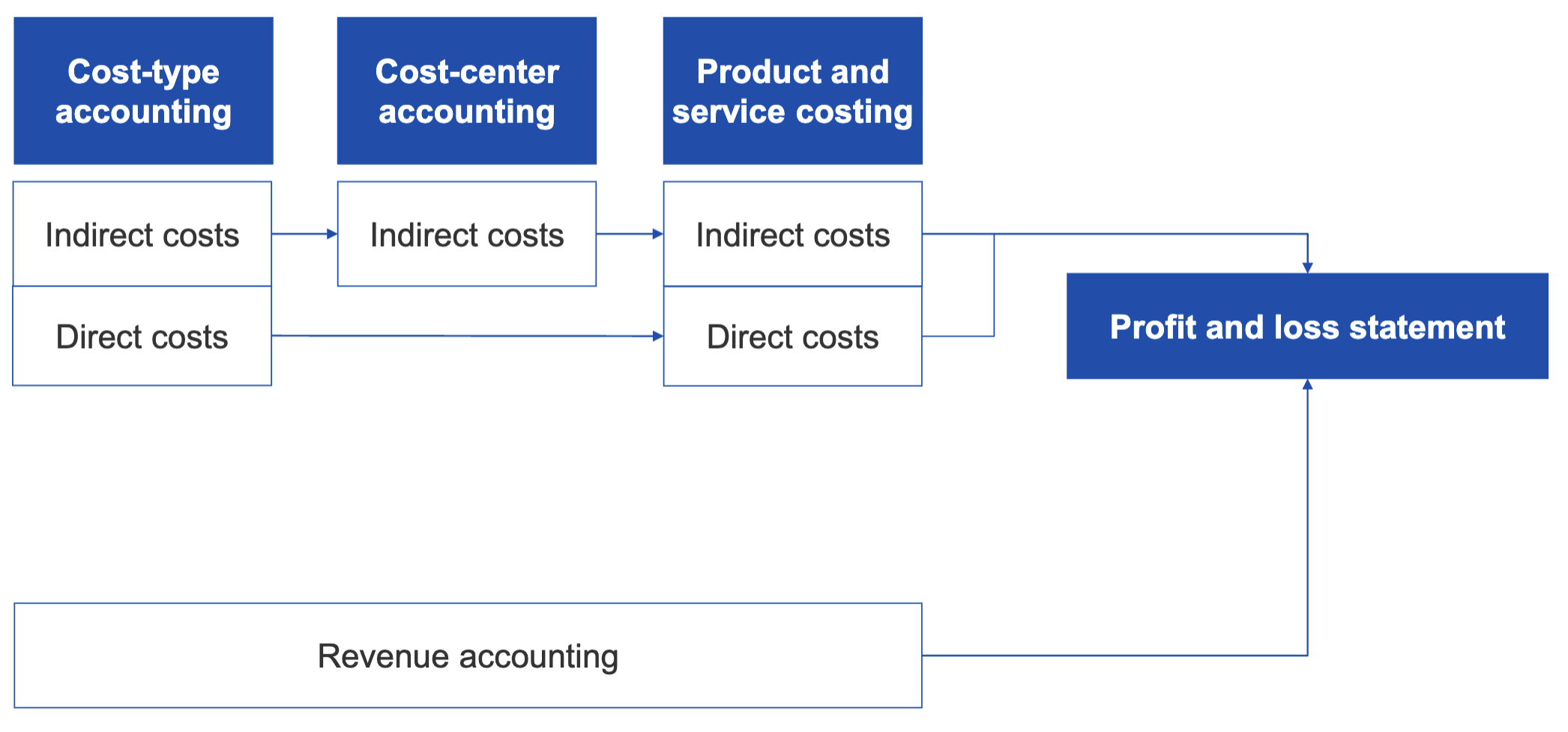

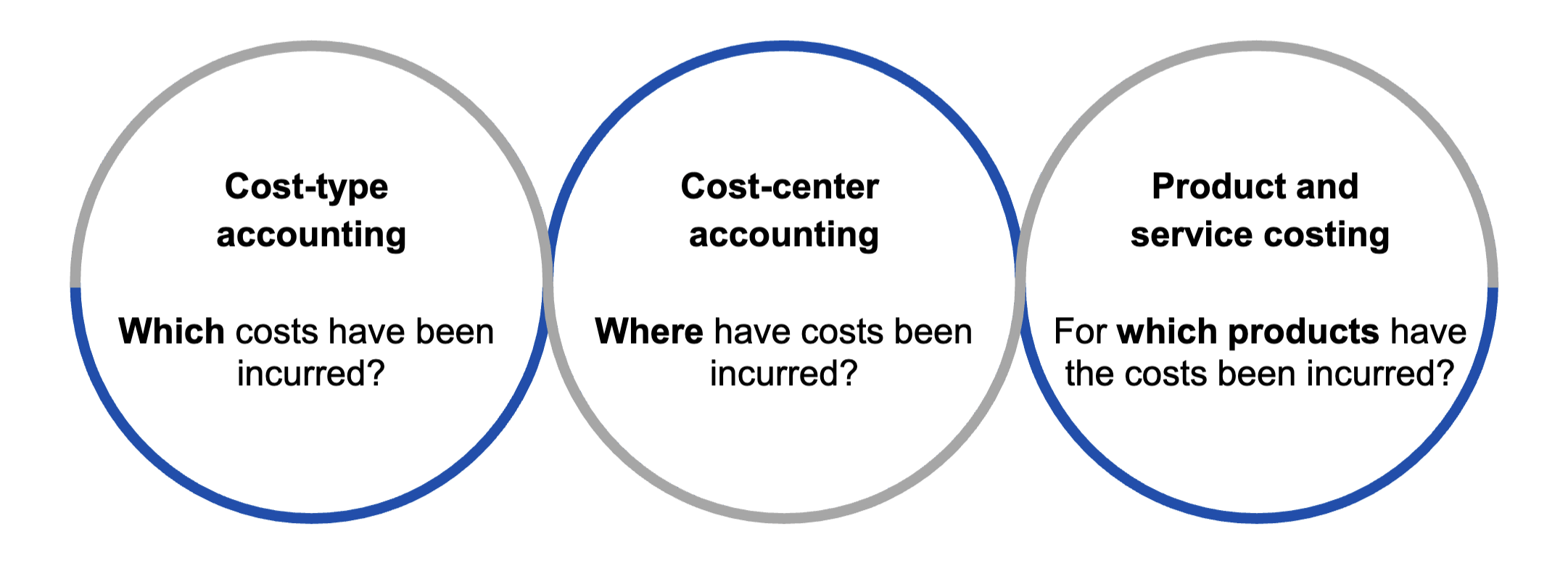

Subsystems of Cost Accounting

Cost-Type Accounting

This answers the question of which costs have been incurred, for example by categorizing costs into types such as direct materials, direct labor, and manufacturing overhead. It provides a detailed breakdown of costs by type, helping to understand the cost structure of production.

More in Cost-Type Accounting.

Cost-Center Accounting

This answers the question of where have costs been incurred, by assigning costs to specific cost centers such as departments, projects, or activities. It helps in tracking and controlling costs within different areas of the organization. In Germany, a typical cost center size is about 10 employees.

More in Cost-Center Accounting.

Product/Service Costing

This answers the main question of many cost accounting systems: for which products have the costs been incurred, by assigning costs to specific products or services. It helps in determining the cost of goods sold, setting prices, and evaluating profitability.

More in Product and Service Costing.