Hand-crafted by Flo, auto-checked by AI.

Resources

Cost-Center Accounting is a method of cost accounting that focuses on the costs incurred in specific departments or units within an organization, known as cost centers. It helps organizations understand where costs are being incurred and how they can be managed effectively. German companies tend to have many small cost centers and manage them detailedly. It answers the question: Where have costs been incurred?

Defining Assigning Cost Centers

Cost centers can be defined based on business function (material, manufacturing, administration), or how costs are allocated (indirect, direct). They should fulfill 4 requirements:

- Homogeneity: Costs within a cost center should be similar in nature.

- Matching Responsibility: Costs should be allocated to cost centers that are responsible for them.

- Completeness and Clarity: All costs should be allocated to cost centers, and the allocation should be clear and understandable.

- Cost-Benefit Criterion: Costs centers should only be created if the benefits of having them outweigh the costs of maintaining them.

Indirect cost centers do not perform their activities directly for the finished products, but for other (indirect and direct) cost centers.

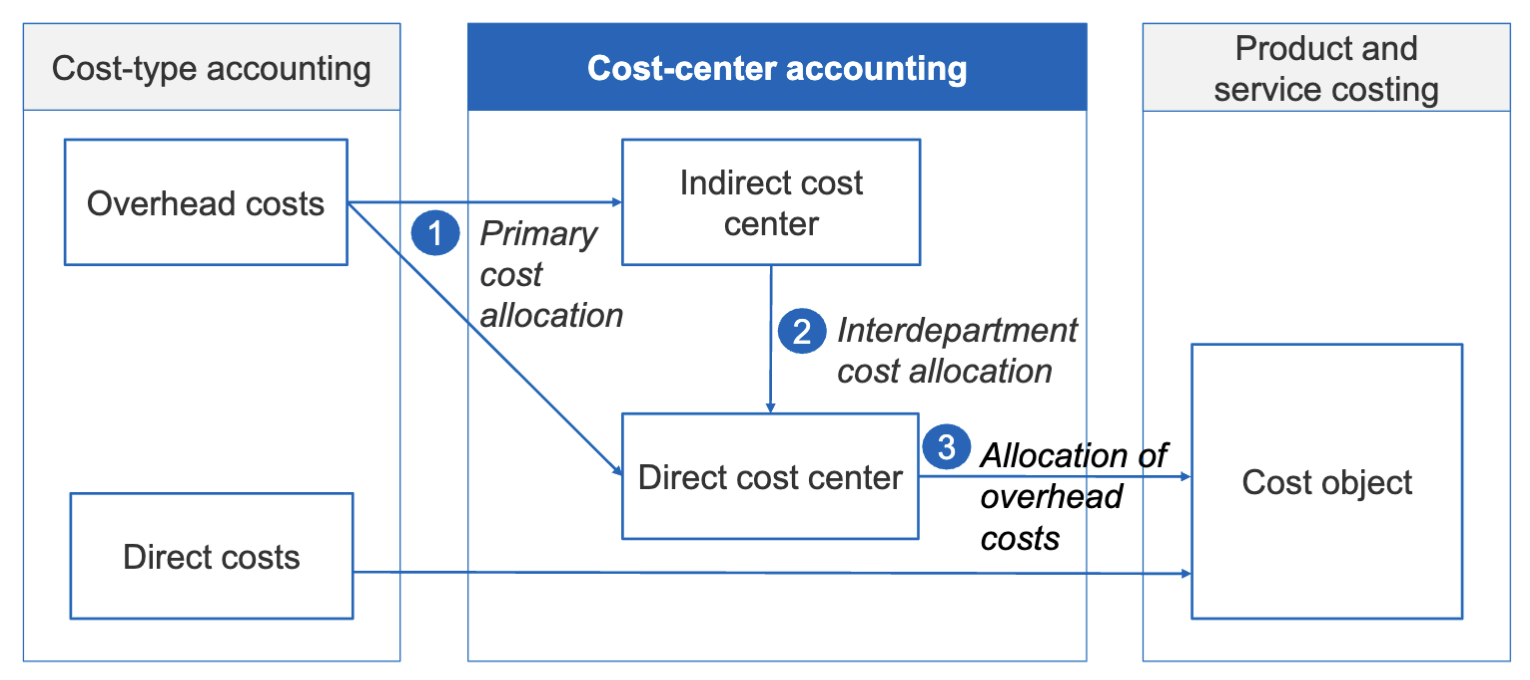

Steps of Cost-Center Accounting

While direct costs can be assigned directly to a cost object, indirect costs require a more complex allocation process. This typically involves three main steps: primary cost allocation, interdepartment cost allocation, and allocation of overhead costs.

This ist usually done using a mapping table from cost type to cost center.

1: Primary Cost Allocation

Firstly, overhead costs are assigned to cost centers based on actual cost drivers, such as labor hours or machine hours. This involves identifying the cost drivers for each cost center and allocating costs accordingly. Costs that can be traced directly to a cost center (e.g. salary) are allocated to the according direct cost center, where as costs that cannot be traced directly (e.g. auxiliary wages) are allocated to indirect cost centers.

To allocate indirect costs, the cost drivers have to be measured either

- Quantity-Based, such as room or energy costs in square meter / watt hours, or

- Value-Based, such as administrative costs based on the value of goods produced.

2: Interdepartment Cost Allocation

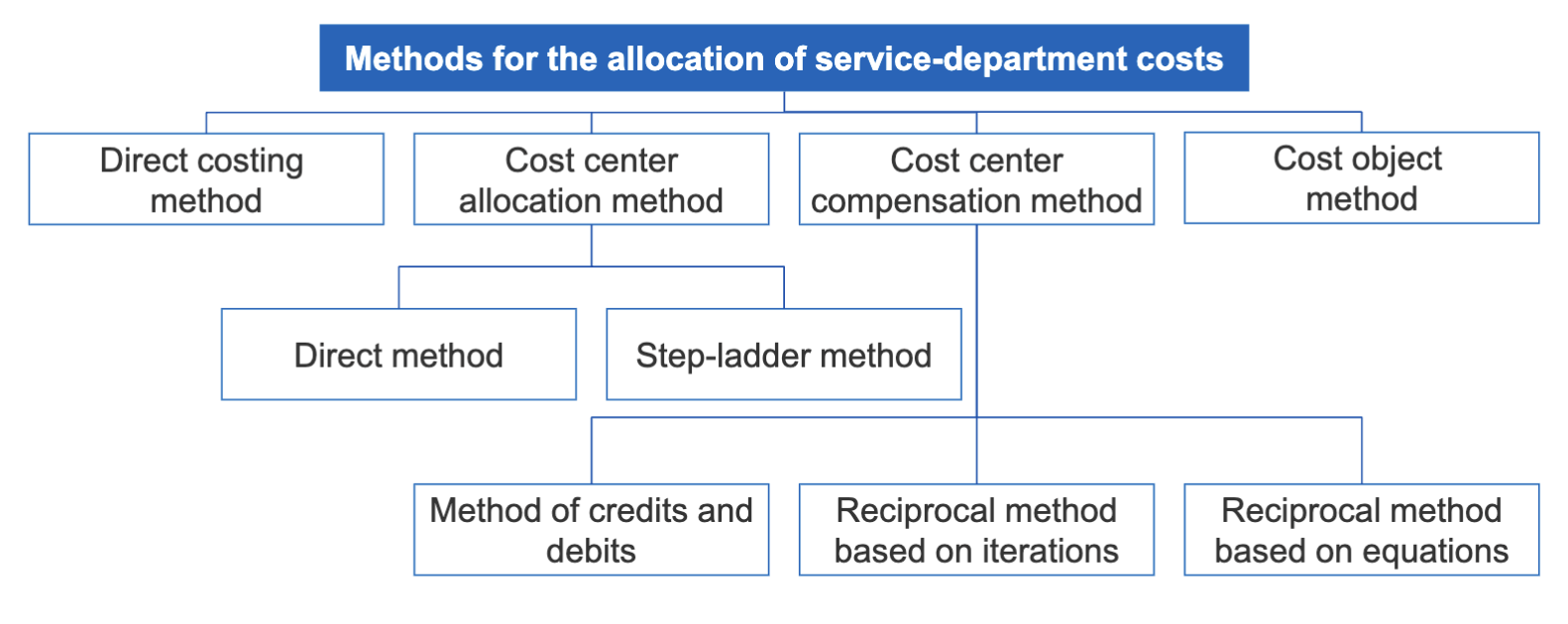

This step allocates costs between cost centers, especially for shared services or support departments. Either from indirect to direct centers, or to another indirect center. There are four main methods with different implementations each, however, this lecture focuses on the cost center compensation method. This method can be implemented exactly using equations, heuristically based on iterations, or pragmatically using credits and debits.

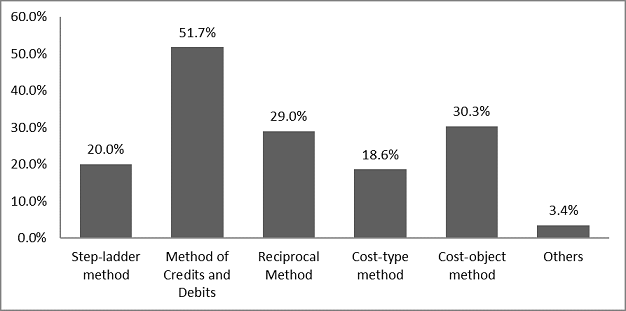

Cost center allocation methods tend to be simpler and are therefore commonly used in smaller enterprises. For companies built on SAP, the compensation method based on iterations is often used.

Distribution amongst German industrial companies:

Equation-Based Reciprocal Compensation

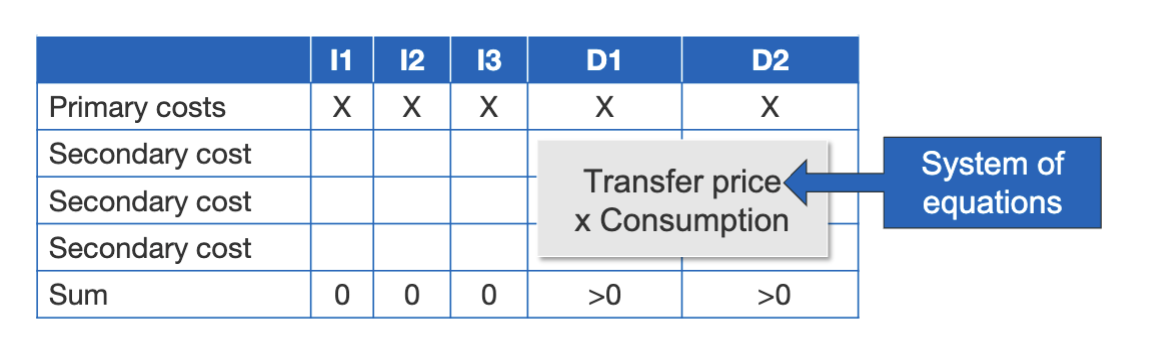

The reciprocal method based on equations is the most (and only exactly) accurate method for allocating costs between cost centers. It involves setting up a system of equations that represent the relationships between cost centers and solving them to determine the allocation of costs. This method takes into account the interdependencies between cost centers and provides a precise allocation of costs. However, recording all internal service exchanges is complex and transfer prices must be recalculated periodically.

| Concept | Determination of transfer prices by solving a system of equations |

| Accuracy | Exact method |

| Recording Effort | All internal exchanges of services |

| Transfer Prices | Transfer prices (or total costs) must be recalculated periodically |

| One equation is formulated for each indirect cost center to achieve a sum of 0: |

In other words: total cost of debt equals primary cost + costs received from other indirect cost centers, and all services must be provided to other cost centers.

where:

- is the number of indirect cost centers with indexes and ,

- is the primary overhead cost of indirect cost center , and its total volume of services

- is therefore the volume of services provided by cost center to cost center

- and are the cost rates of cost centers and , respectively.

Aside

The system of equations is solved to find the transfer rate of each indirect cost center, which can then be multiplied by the quantity of services provided to direct cost centers to determine the total cost allocated to each direct cost center.

An example is available on slide 88.

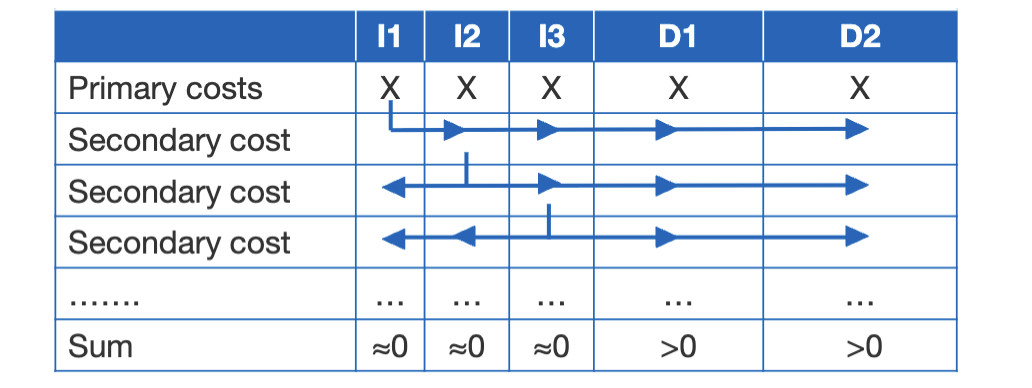

Iteration-Based Reciprocal Compensation

For larger companies with many cost centers, the equation-based method is too computationally expensive. The iteration-based method is a heuristic approach that approximates the solution by iteratively allocating costs until the changes in allocated costs become negligible. This method is less accurate than the equation-based method but is more scalable.

| Concept | Repeated allocation of the costs for internal services in several steps |

| Accuracy | Approximation; accuracy increases with number of iterations |

| Recording Effort | All internal exchanges of services |

| Transfer Prices | Determination of transfer process for allocation of service exchanges not necessary |

Aside

First, all costs of the first indirect cost center are allocated to the other cost centers, then the costs of the second indirect cost center are allocated, and so on. Doing this, pay attention to costs allocated to the inspected center by a previously inspected center.

After one round of allocation, the costs of indirect cost centers have changed, so the process is repeated until the changes in allocated costs become negligible.

An example is available on slide 92.

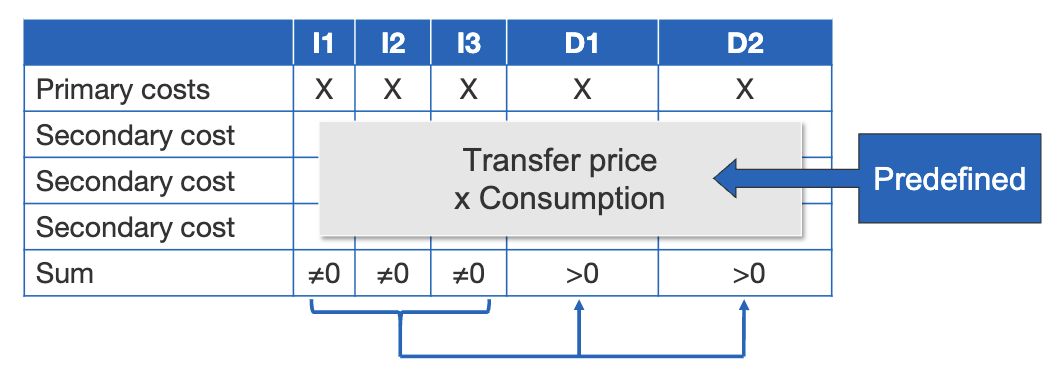

Credit/Debit-Based Compensation

This method is a more pragmatic approach that uses credits and debits to allocate costs between cost centers. This method is less accurate than the other two methods but is simpler to implement and requires less recording of internal service exchanges. It assumes that transfer costs are known roughly.

| Concept | Assumption that transfer prices for internal services already exist |

| Accuracy | Approximation, accuracy depending on the transfer prices used |

| Recording Effort | All internal exchanges of services |

| Transfer Prices | Transfer prices are predefined |

Aside

Implementing this method is simple: for each internal service exchange, the providing cost center is credited with the transfer price, and the receiving cost center is debited with the same amount. This process is repeated for all internal service exchanges until all costs have been allocated.

The sum of indirect costs does not usually resolve to 0, as transfer price assumptions are not exact. Therefore, an additional step is required to allocate the remaining costs, which can be done by estimation.

Given an allocation to another center, simply divide by the service quantity to identify the transfer price.

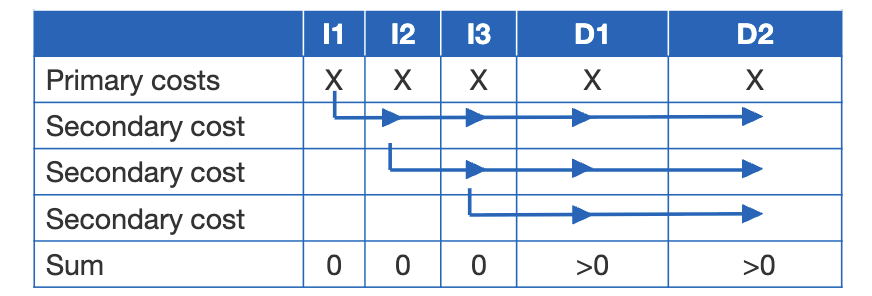

Step-Ladder Allocation

The step-ladder method is a simplified approach to interdepartment cost allocation that allocates costs in a sequential manner, starting with the cost center that provides the most services to other cost centers. This method is less accurate than the other methods but is easier to implement and requires less recording of internal service exchanges. It’s only exact if all services between indirect cost centers are one-sided.

| Concept | Consideration of services between indirect cost centers, but only in one direction |

| Accuracy | Exact, if only one-sided exchanges of services exist between indirect cost centers, otherwise only approximate |

| Recording Effort | Internal exchanges of services in one direction only |

| Transfer Prices | Transfer prices must be recalculated periodically; the amount of transfer prices varies according to the sequence of the settled indirect cost centers |

Aside

In the first step, the costs of the indirect cost center that provides the most services to other cost centers are allocated to the other cost centers, with the usual transfer price of . In the second step, the costs of the next indirect cost center are allocated – respecting costs already allocated to this center, and excluding services delivered to cost centers already inspected – and so on. This process is repeated until all indirect cost centers have been allocated.

Direct Allocation

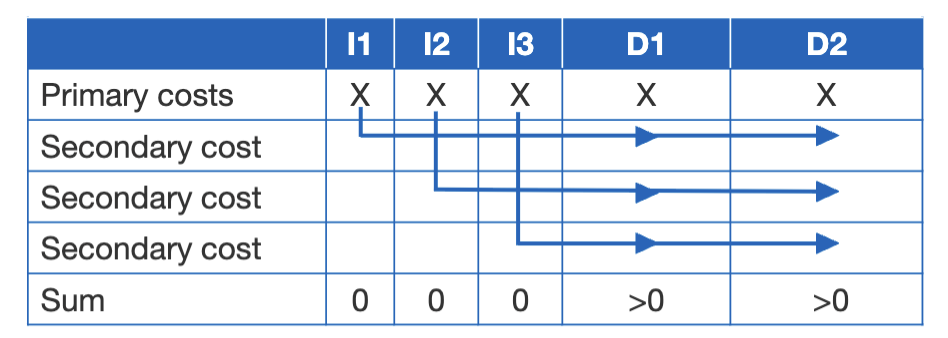

The simplest of the methods considered in this module. Direct allocation ignores any services provided between indirect cost centers and allocates costs directly to direct cost centers based on the primary cost allocation. This method is less accurate than the other methods but is easier to implement and requires less recording of internal service exchanges. It’s only exact if no services between indirect cost centers exist.

| Concept | No consideration of exchanges of services between indirect cost centers |

| Accuracy | Exact, if no exchanges of services exist between the indirect cost centers, otherwise only approximate |

| Recording Effort | Internal exchanges of services only at direct cost centers |

| Transfer Prices | Transfer prices must be recalculated periodically; relation of primary costs and activity output to direct cost centers |

Aside

Clearly, only services provided to direct cost centers are part of the transfer price calculation. As usual, the transfer cost is determined by dividing the primary cost of the indirect cost center by the quantity of services provided to direct cost centers.

3: Allocation of Overhead Costs

The final step allocates costs from direct cost centers to specific cost objects to determine overhead rates for costing the product or service. Different allocation bases to determine what share of indirect costs is allocated to each cost object can be used, for example the object’s direct cost. These options are covered in Product and Service Costing.

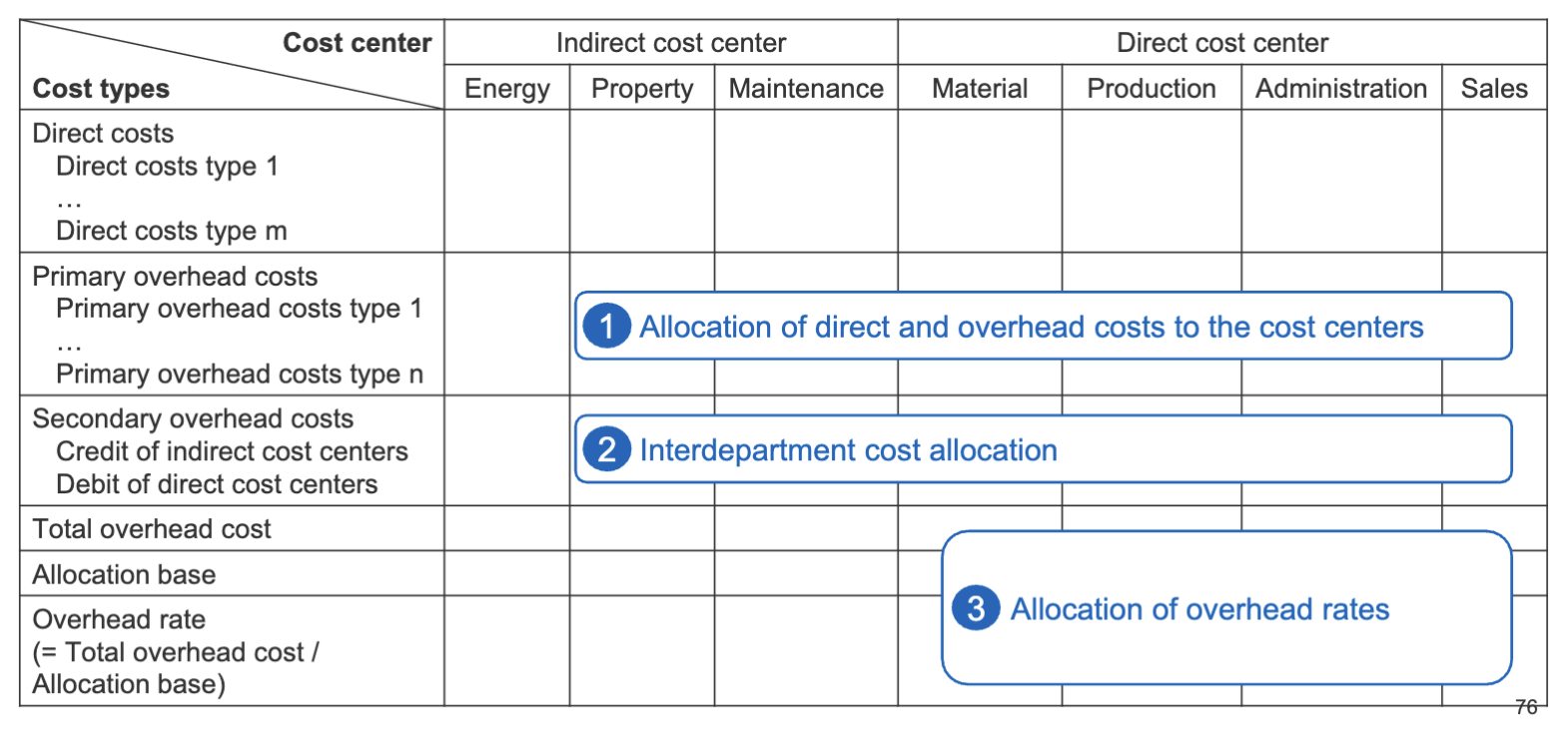

Example table of overhead costs after step 2 (interdepartment cost allocation):

The overhead is given by dividing the total overhead cost by the allocation base, in this example the direct cost.