Hand-crafted by Flo, auto-checked by AI.

Resources

To determine the optimal mix of debt and equity financing, companies must analyze the trade-offs between the benefits and costs of debt. The Modigliani-Miller theorem provides a framework for understanding how capital structure affects a company’s value under certain assumptions.

Capital Structure

Modigliani-Miller Theorems

In a perfect capital market with no taxes, transaction costs, or bankruptcy costs:

- Theorem 1 states that the value of a leveraged firm is the same as an unleveraged firm:

Market value of equity and debt in a levered firm equals the market value of equity in an unlevered firm, which equals the total value of the firm’s assets.

Otherwise, there would be an arbitrage opportunity (law of one price). Additionally, homemade leverage would otherwise allow investors to replicate the effects of corporate leverage on their own, making corporate leverage irrelevant, restoring equilibrium.

- Theorem 2 states that the cost of equity increases with leverage, such that the weighted average cost of capital (WACC) remains constant regardless of the capital structure:

The cost of equity (r_E) equals the cost of unlevered equity (r_U) plus a leverage premium that increases with the debt-to-equity ratio (D/E) and the spread between the cost of unlevered equity and the cost of debt (r_U - r_D).Therefore, if capital structure affects firm value in the real world, it must be due to market imperfections such as taxes, bankruptcy costs, or agency costs.

The Modigliani-Miller theorem assumes that all investors have equal information and expectations, firms in the same risk class face the same borrowing costs, cash flows are perpetual, and that there’s a perfect capital market.

Perfect Market

A theoretical market where:

- Investors and firms can trade a set of securities at competitive market prices equal to the present value of their future cash flows.

- There are no taxes or transaction/issuing/agency costs associated with security trading.

- A firm’s financing decisions do not change the cash flows it generates or reveal any information about its future prospects.

Leverage Effect

The leverage effect refers to how the use of debt financing can amplify returns for equity holders.

- Leverage amplifies returns when project/asset returns exceed the cost of debt ()

- Leverage amplifies risk symmetrically, increasing both upside and downside potential

- The leverage effect is mechanical, not value-creating

Impacts on Risk

The equity beta equals the asset beta plus a leverage premium that increases with the debt-to-equity ratio. The underlying business risk (asset beta) stays constant, but leverage amplifies this risk for equity holders, raising equity beta. Capital structure does not affect total firm risk but does affect how that risk is distributed between debt and equity.

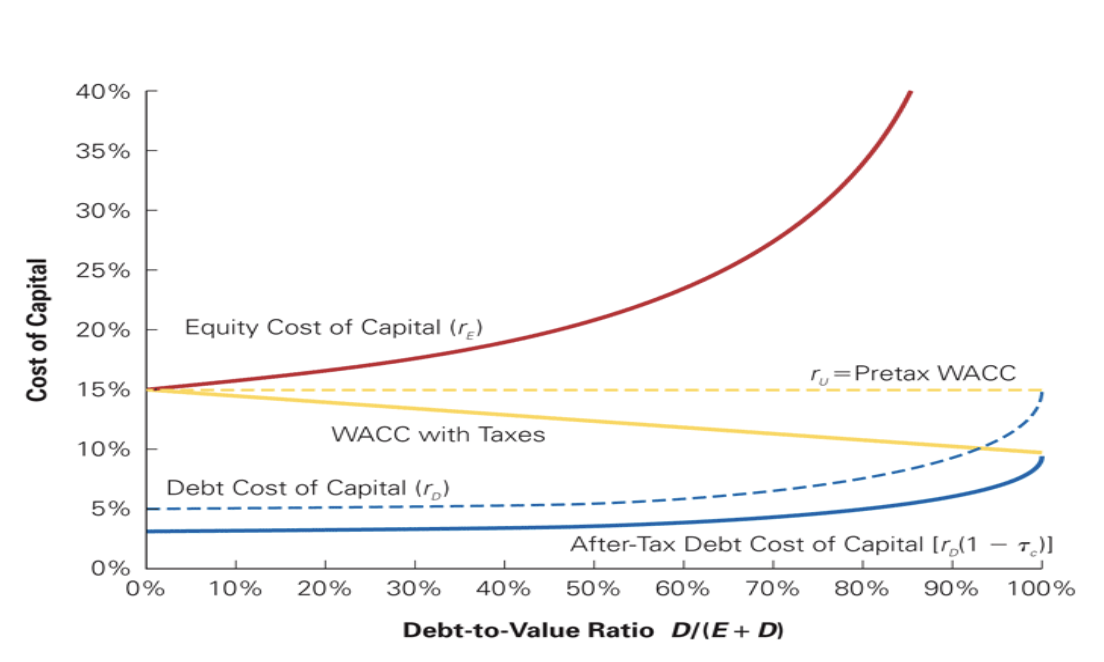

Tax Shield

The reason capital structure affects firm value in the real world is primarily due to the tax deductibility of interest payments. From a financing decision, interest payment is value creation because cash that would’ve gone to the government stays with the investors.

Therefore, WACC decreases as leverage increases (effective after-tax cost of debt is lower than pre-tax), and therefore the firm value increases. The value of a levered firm exceeds the value of an unlevered firm by the present value of the tax shield:

For permanent debt at interest rate , the annual tax shield is , which yields:

The tax-adjusted WACC is:

(See WACC with Taxes)

Tax Shield Limits

The tax shield only works if the firm generates sufficient taxable income to utilize it. If the firm has higher interest expenses than taxable income (EBIT), it cannot fully benefit from the tax shield. Since EBIT is usually uncertain, the expected value of the tax shield is less than .

Downsides of Leverage

High leverage creates cost due to the risk of financial distress. Financial distress brings direct costs (legal fees, administrative expenses) and indirect costs (lost customers, restricted credit access, forgone investment opportunities, employee departures).

High leverage also creates conflicts of interest between debt and equity holders, causing agency costs (e.g., risk-shifting/asset substitution and debt overhang/underinvestment) because debt holders have a senior claim on assets while equity holders have limited liability.

Balancing these forces is key to determining the optimal capital structure: Firms increase debt to capture tax benefits up to the point where the marginal tax advantage is offset by the marginal expected costs of financial distress and agency conflicts.

Leverage and Beta

In the relationship between leverage and beta, several key insights emerge:

- Asset Beta () is Constant: Financial leverage does not change the total systematic risk of the firm’s underlying business operations. The asset beta (or unlevered beta) remains constant regardless of the capital structure:

- Leverage Amplifies Equity Beta (): Financial leverage redistributes systematic risk away from debt holders and concentrates it into equity. As the debt-to-equity () ratio increases, equity beta rises in a predictable, linear way:

- Mathematical Split: The levered equity beta consists of two parts: the base operational risk () plus a leverage risk premium ().

- Buffer Effect of Cash: Significant cash holdings act as a risk buffer. Because cash has a beta of zero, high cash balances result in a negative net debt, which drives the equity beta below the operational asset beta (see [[Cost of Capital#Estimating for New Projects|safe cash cushion]]).

- High Leverage Limitation: At extreme leverage levels, debt itself becomes risky, causing the debt beta () to rise. Consequently, the further escalation of equity beta slows down because debt holders begin sharing some of the systematic risk.