Resources

Bonds

The most important bond is the US Treasury bond, which is issued by the US government. Contrary to Stocks, there are many influencing factors to design a bond, such as the maturity date, the coupon rate, and the face value.

- Principal: The face value of the bond, which is the amount the bondholder will receive at maturity

- Maturity date: The date on which the bond will mature, and the bondholder will receive the face value

- Coupon rate: The fixed percentage of the face value that the bondholder receives as interest each year

- Yield to Maturity (YTM): The discounted yearly return to the bond, which is influenced by the coupon rate, the purchase price, and the time to maturity.

- Bond Price: A bond’s market price is usually measured as a percentage of the principal

Premiums and Discounts

When the bond price is above 100%, as in markets will pay more than the face value, this is called a premium. When the bond price is below 100%, it is called a discount.

There are two major types of bonds:

- Coupon Bonds: Pay periodic interest (coupons) to the bondholder, usually semi-annually or annually, until maturity. At maturity, the bondholder receives the face value of the bond.

- Zerobonds: Do not pay any interest, but are sold at a discount to their face value. The investor receives the face value at maturity, which includes the interest.

- Bonds with variable interest: Coupon payments are adjusted to current interest level (LIBOR)

- Perpetual Bonds (Consol Bonds): Do not have a maturity date and pay interest indefinitely; often issued by governments

- Convertible Bonds: Bond with small coupon that provide the possibility to be exchanged against stocks at a predetermined date in time

- Option Bonds: Like convertible bonds, but option right is traded separately at maturity

For pricing, the general present value formula applies, where the cash flows are the coupon payments and the face value at maturity, discounted at the yield to maturity. The price of a bond can be calculated as the sum of the present value of all future cash flows.

Pricing Coupon Bonds

Coupon bonds pay periodic interest (coupons) to the bondholder, usually semi-annually or annually, until maturity. The coupon rate is the fixed percentage of the face value that the bondholder receives as interest each year. At maturity, the bondholder receives the face value of the bond.

The price of a bond given coupon rate , principal , and desired yield to maturity is:

Beyond Constant Rates

The formula above and influences below assume a parallel shift in a constant interest rate . For realistic pricing where interest rates vary by maturity, see Sloping Yields Curves.

Coupon and Redemption Influences

The higher the coupon and redemption payment, the higher the market price of the coupon bond.

Additionally, prices are impacted by compensation to the seller (dirty price), with a settlement amount of:

Buy Clean, Pay Dirty

When a bond is purchased between coupon payment dates, the buyer must pay the seller the accrued interest since the last coupon payment. “Buy clean, pay dirty” means that the buyer pays the clean price of the bond plus the accrued interest.

Maturity Influences

Price typically approaches nominal as the bond approaches maturity, since the present value of the remaining coupon payments decreases as time goes on. Therefore, the discounting effect of market rates higher than coupon rates (and premium the other way) is larger for bonds with longer maturities, and smaller for bonds with shorter maturities.

Interest Level Influences

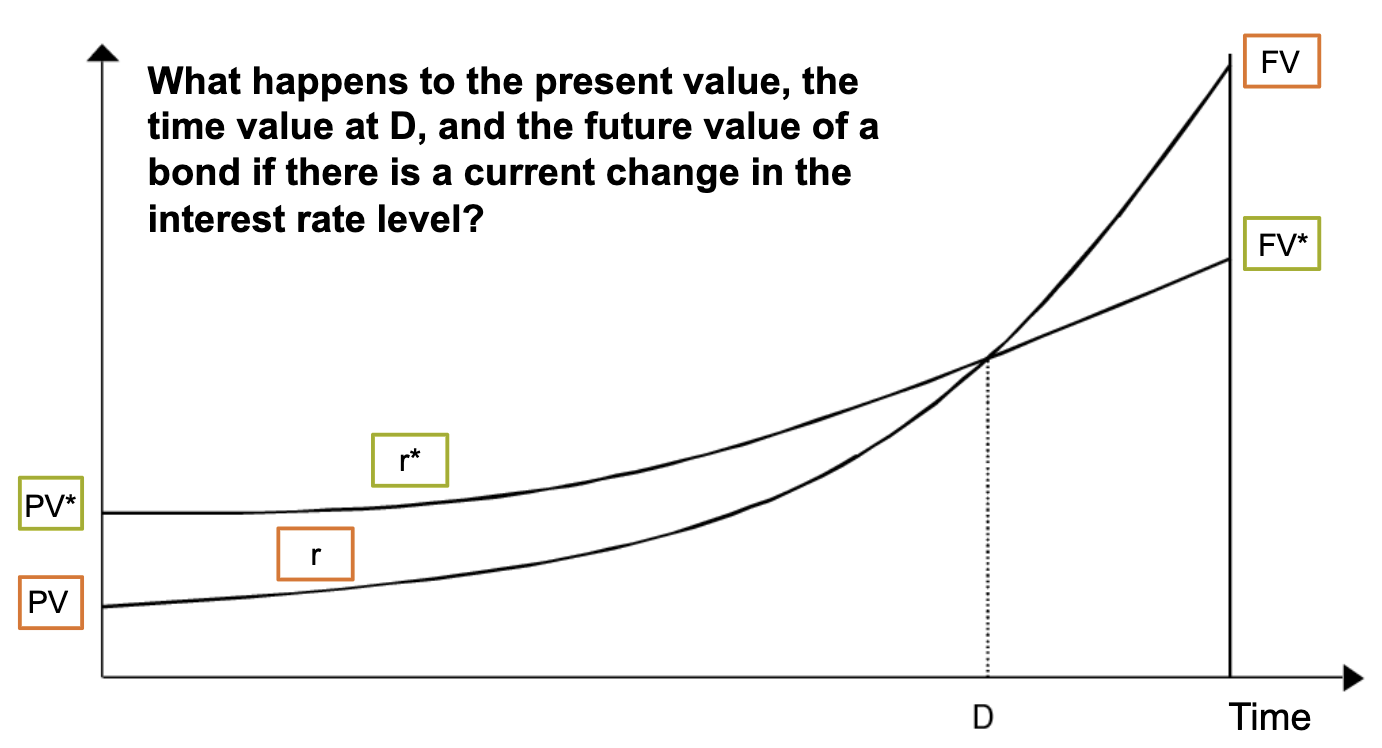

If the market interest rate increases, the price of existing bonds decreases, and if the market interest rate decreases, the price of existing bonds increases. This is because the fixed coupon payments of existing bonds become less attractive when market rates rise and more attractive when market rates fall.

If the bond is held until maturity, cash flow does not depend on the interest rate, but the price of the bond will fluctuate with changes in market interest rates. If the bond is sold before maturity, the price at which it can be sold will depend on the prevailing market interest rates at that time.

Pricing Zerobonds

Zerobonds are sold at a discount to their face value, and the investor receives the face value at maturity. The difference between the purchase price and the face value represents the interest earned by the investor.

The price of the zerobond given the principal and the desired yield to maturity is:

Like the coupon bond pricing formula, this formula assumes a constant discount rate. See below for the adjusted formula.

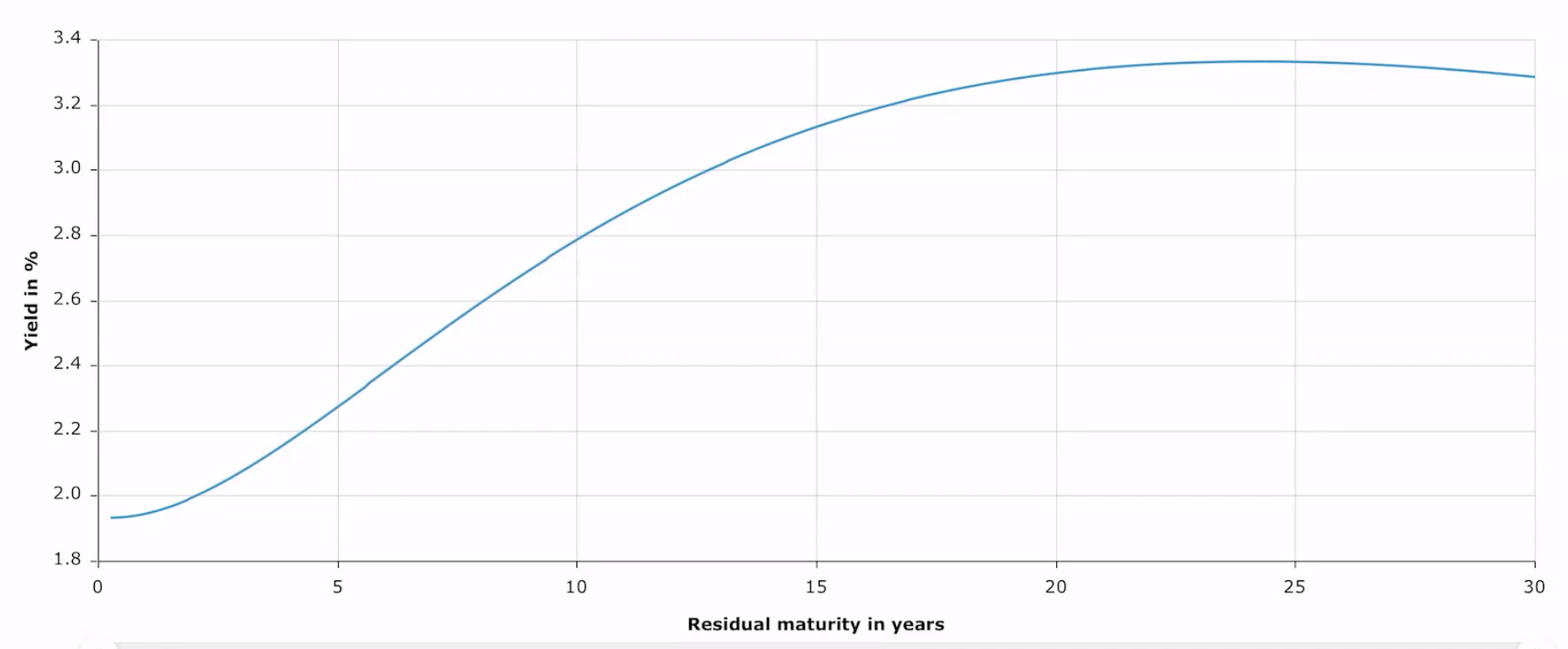

Sloping Yields Curves

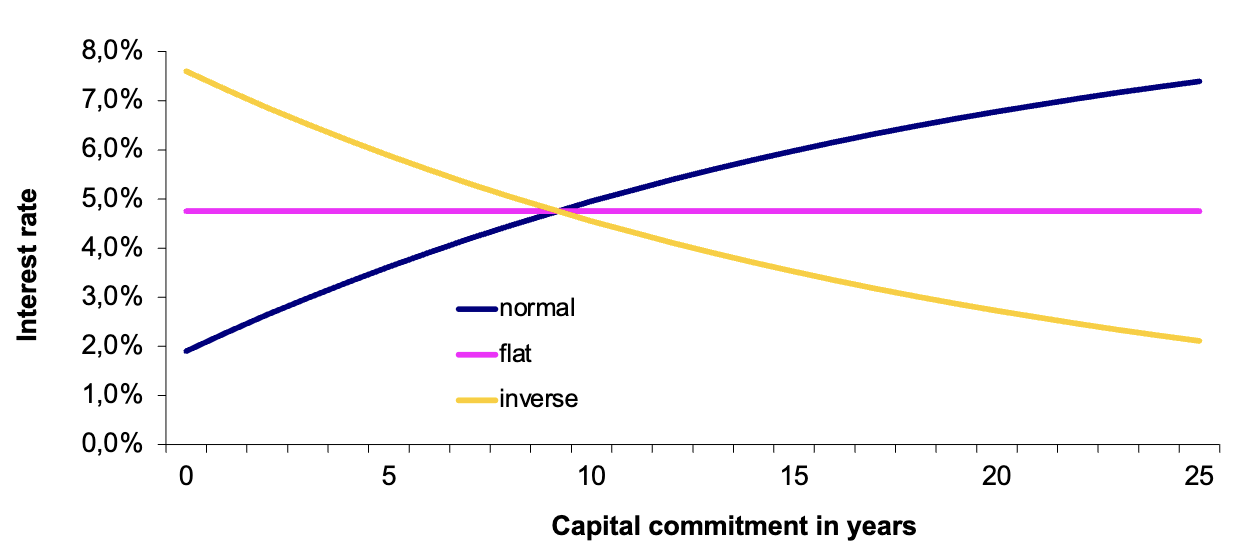

Market interest rates differ based on the time to maturity. This relationship is defined by the term structure of interest rates (the yield curve), with one series per interest rates for corresponding commitment periods.

- Normal yield curve: The longer the capital commitment, the higher the paid interest rate.

- Flat yield curve: Paid interest does not depend on the time of capital commitment.

- Inverse yield curve: The longer the capital commitment, the lower the paid interest rate.

The yield curve is also called spot curve:

Inverse term structures are often observed just before a recession, as investors expect interest rates to fall in the future. For the normal yield curve, different theories explain the shape of the curve (which are interesting but do not seem relevant for the exam):

- Pure Expectation Hypothesis: The shape of the yield curve is determined solely by what the market expects future short-term interest rates to be.

- Liquidity Preference Theory: Long-term bonds must pay a higher rate than short-term bonds to compensate investors for the increased risk of locking up their capital.

- Market Segmentation Theory: Interest rates for different maturities are set entirely by the independent supply and demand forces within specific institutional borrower and lender groups.

Spot Rates and Forward Rates

- Spot Rate (): The periodic market interest rate valid for a commitment starting today () and ending at a future maturity date (). It is used to discount single cash flows at that specific maturity.

- Forward Rate (): The periodic interest rate for a specific future period (e.g., from to ), contractually locked in based on information and rates available today ().

- The long-term spot rate () can be seen as the average annual rate, reproducing the same return as investing in a sequence of forward rates (the geometric mean of current spot and the forward rates). This is required by the no-arbitrage condition.

The relationship between long-term spot rates and forward rates is simply given by:

Note that works like , but with multiplication instead of addition.

The same no-arbitrage condition applies to multi-year periods starting in the future, so that investing once at must yield the same return as investing first at and then at :

While forward rates determine future spot rates in theory, they are not practically a useful predictor of future interest rates. They are more useful for pricing and hedging than for forecasting.

Calculations

Determining a 1-Year Forward Rate from Spot Rates:

This is simply the ratio of the returns from investing in a at the spot rate until versus the rate until 1 year before that.

Determining a Multi-Year Forward Rate from Spot Rates:

If starting today, (terms become and ). This is the geometric average of the returns from investing in a long-term spot rate versus a shorter term spot rate.

Yield to Maturity with Sloping Curves:

When the yield curve is not flat, the YTM is an average summary metric and cannot be used to discount individual cash flows. Instead, each cash flow must be discounted using its individual spot rate. The price of the bond can be calculated by discounting each cash flow with its corresponding spot rate and then equating that price to the constant-rate formula to solve for the YTM.

- Find actual market price () by discounting every cash flow with its individual spot rate (:

- Equate that price to the constant-rate formula to solve for the YTM ():

Risks

Bonds are often considered less risky than Stocks (because of the fixed payments and priority in case of bankruptcy), but they are not risk-free. The main risks associated with bonds include:

- Credit Risk: The risk that the issuer of the bond will default on its payments. This risk is higher for corporate bonds than for government bonds.

- Price Risk: The risk that changes in market interest rates will affect the price of the bond. When interest rates rise, bond prices fall, and when interest rates fall, bond prices rise.

- Risk of Reinvestment: The risk that interest rates are lower when coupons are received than when the bond was purchased, leading to lower returns when reinvesting those coupons.

Interest rate risk and risk of reinvestment work similarly, but in opposite directions. Additionally, there are risks of liquidity (the risk that the bond cannot be sold easily without a significant price reduction) and inflation (the risk that the purchasing power of the bond’s future payments will be eroded by inflation).

Credit Risk

Credit rating agencies like Standard & Poor’s or Moody’s provide ratings for bonds based on the issuer’s creditworthiness. These ratings range from AAA (highest quality) to D (default). Bonds with lower ratings typically offer higher yields to compensate investors for the increased risk of default.

Credit Ratings Context

Industrial companies often have A or BBB ratings, while financial institutions often have lower ratings due to their higher leverage. Government bonds typically have higher ratings, with German bonds currently still rated AAA, whereas US treasury bonds have been downgraded.

AAA ratings imply very high equity ratios, which is not desirable from a tax perspective.

Price and Reinvestment Risk

When the market interest rate shifts, it triggers two opposing effects on a bond portfolio:

- Price Risk: An increase in market interest rates leads to a decrease in the bond price (and vice versa). This matters if you want or need to sell the bond before maturity.

- Reinvestment Risk: The risk that future cash flows (incoming coupon payments or the final principal) must be reinvested at lower market interest rates, dragging down long-term total wealth.

The Trade-off:

- If market interest rates decrease right after purchase: You get a short-term capital gain (bond price goes up), but lower long-term returns on reinvested coupons.

- If market interest rates increase right after purchase: You suffer a short-term capital loss (bond price drops), but benefit from higher long-term returns on reinvested coupons.

Duration

Duration (or Macaulay Duration) identifies the exact point in time where price risk and reinvestment risk perfectly offset each other (the the average commitment period of the investment). If an investor holds the bond for exactly this duration, they are fully immunized against interest rate risk; their total wealth at that specific target date will not depend on market interest rate fluctuations.

Mathematical Derivation

Macaulay Duration (): The present-value-weighted average time to receive all cash flows. It represents the required holding period for full interest rate immunization.

Modified Duration (): Adjusts Macaulay duration to serve as a direct measure of percentage price sensitivity to a change in interest rates.

Sensitivity to Interest Rates

The interest rate sensitivity (and thus the duration) of a bond changes depending on its underlying contractual features and the market environment:

- Zero-coupon bonds (Zerobonds): Duration equals exactly the maturity of the bond (), because there are no intermediate coupon payments to pull the cash flow weight forward.

- Perpetuals (Consol Bonds): For bonds without a maturity date, duration does not grow infinitely but converges to a distinct limit value:

For typical coupon-bearing bonds, three main variables dictate the size of duration and exposure to interest rate shifts:

| Factor | Shift Direction | Core Financial Logic |

|---|---|---|

| Maturity () | Higher Maturity Higher Duration | The longer the capital commitment period, the further out the heavy final principal repayment lies, increasing the bond’s long-term risk exposure. |

| Market Interest Rate () | Lower Market Rate Higher Duration | Lower discount rates put higher mathematical weight on late cash flows (like the principal at maturity), stretching out the average commitment period. |

| Coupon Rate () | Lower Coupon Higher Duration | Smaller intermediate coupon payments mean less cash is returned early on, shifting the relative weight of the bond’s total present value toward the final maturity date. |