Resources

Annuities

Annuity-immediate and Annuity-due

- Annuity-immediate: Payments at the end of each period (e.g., bond coupons), with the first payment at and last at .

- Annuity-due: Payments at the beginning of each period (e.g., rent), with the first payment at and last at .

Since annuity-immediate lacks behind one period:

Constant Annuities

Constant annuities have fixed payments at regular intervals. The formulas for future value (FV) and present value (PV) depend on whether it’s an annuity-immediate or annuity-due.

Annuity-Immediate:

The second representation of this formula is the most common version.

Where: is the constant payment, is the interest rate, , is the number of periods, and is the future value factor for an annuity-immediate ().

Therefore, to, for example, calculate the required time for a given future value (annuity-immediate):

For annuity-due, multiply by to account for the earlier payments.

For example, when determining the required payment for a given future value, it is one factor of less than for the immediate annuity.

Intra-year Annuities

If interest compounding periods are longer than annuity payment periods, a fictitious annuity is created to match the compounding period (respecting the time value of money, see slide 60):

is always an annuity-immediate, therefore additional formulas use the immediate variant.

Intra-year Compounding

If compounding periods are shorter than annuity payment periods, a fictitious interest rate is created to match the payment period (implies shorthand for continuous compounding, see Continuous Compounding and slide 61):

Payout Phase

Determining the payout value of a pension can be tricky because it depends on the expected lifespan of the pensioner, which is uncertain. We can, however, calculate the payout duration given a certain payout value, by using the present value of an annuity formula, e.g. annuity-immediate:

Similarly, do determine which annual savings rate for years is required to be able to afford a certain annuity-immediate payout for the following years, we can rearrange the formula for the present value of an annuity-immediate to solve for (the payment during the saving phase):

Variable Annuities

Variable annuities have payments that can change over time, often based on an underlying index or investment performance. The formulas for future value and present value of variable annuities depend on the specific payment structure and the underlying assumptions about the variability of payments.

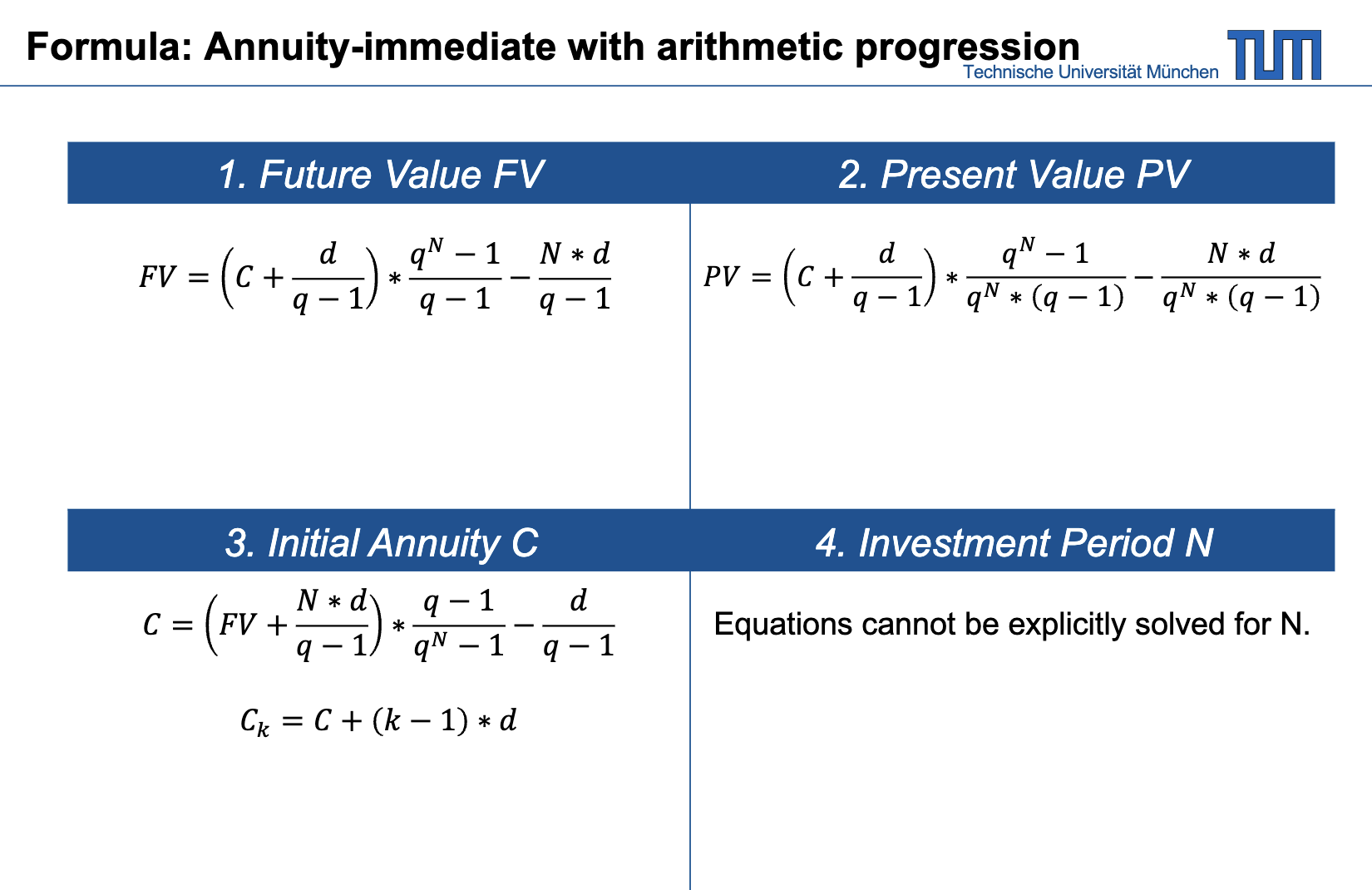

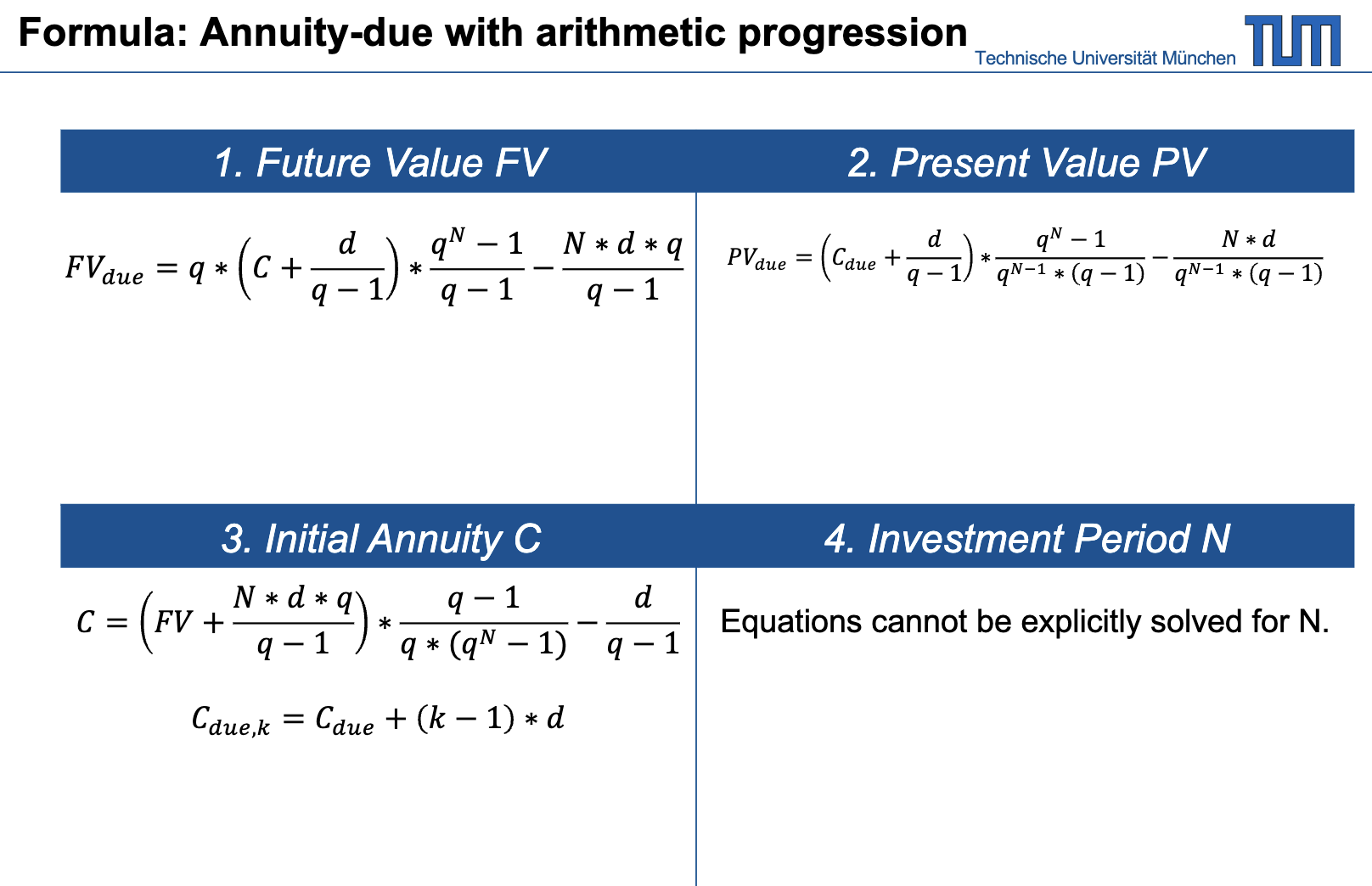

Arithmetic Progression

An arithmetic progression is a sequence of numbers in which the difference between consecutive terms is constant, i.e. , with the payment in period being . The future value of an annuity with payments in arithmetic progression can be calculated using the formula (see slide 68):

and for annuity-due:

same formulas as above:

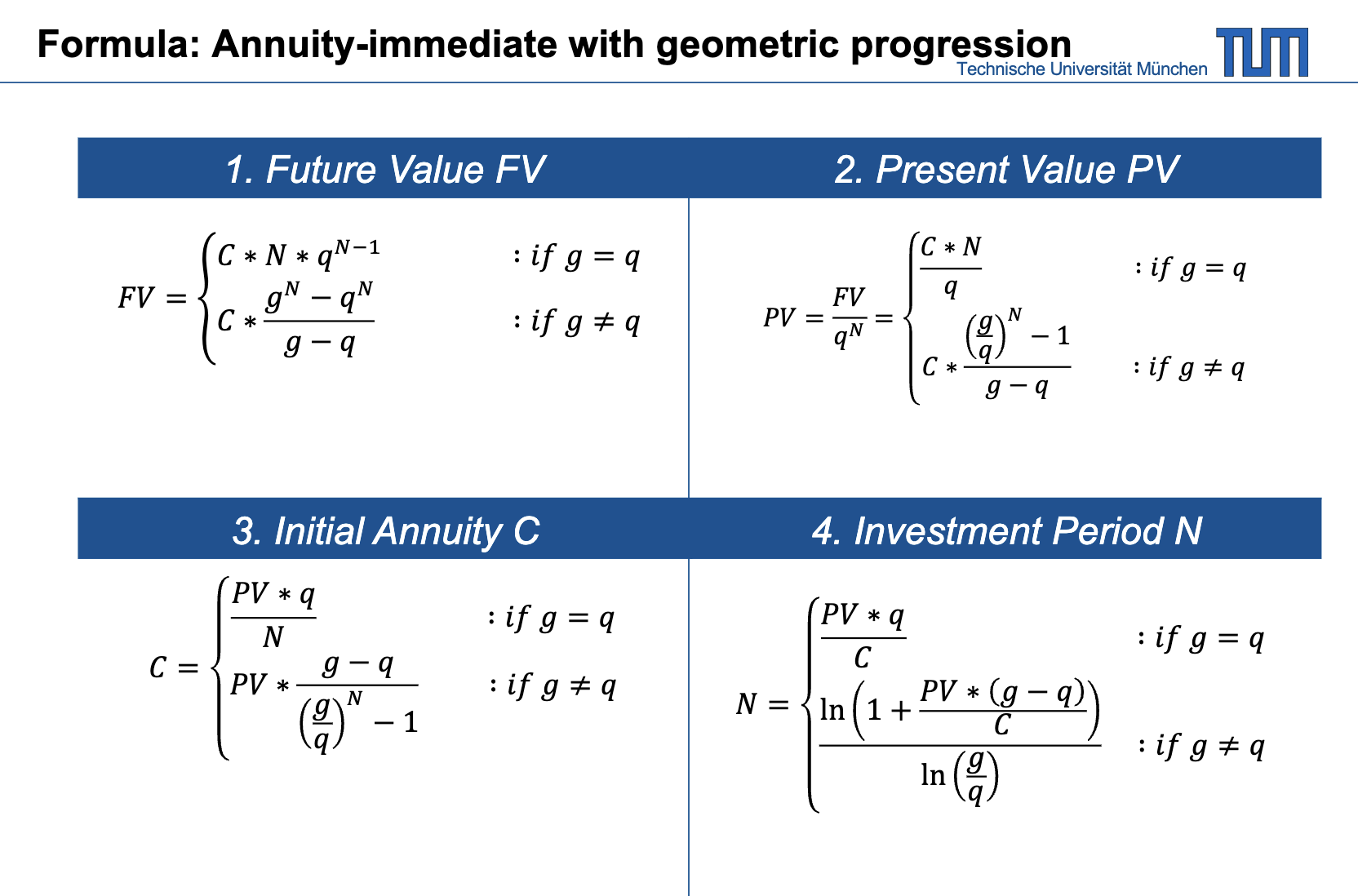

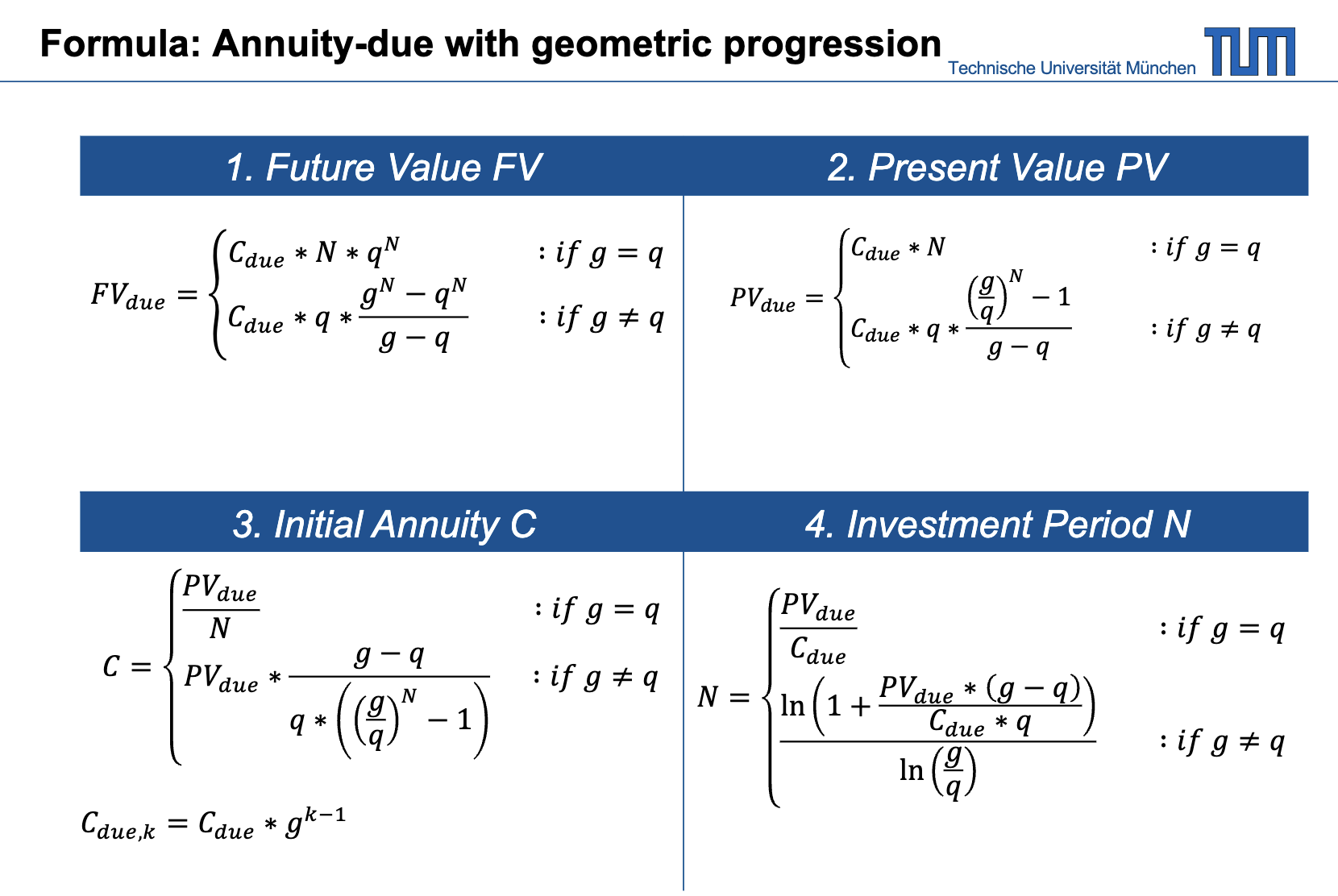

Geometric Progression

Annuities with a geometric progression are more common (e.g. to adjust for inflation), they increase with a constant rate, i.e. , with the payment in period being .

Perpetuities

A perpetuity is a type of annuity that continues indefinitely, with payments that do not end. If the interest factor is larger than the growth factor , the present value converges to a finite number (Gordon growth model):

The future value of an annuity with payments in geometric progression can be calculated using the general formula (see slide 69):

Growth Rate ≠ Interest Rate ()

for annuity-immediate:

and for annuity-due:

Growth Rate = Interest Rate ()

for annuity-immediate:

and for annuity-due:

same formulas as above: