Resources

When companies operate, they constantly make decisions that affect their costs and profitability. To make informed decisions, they need accurate and timely information about their costs, revenues, and profits. This is where operative decision information comes into play.

Decision-Making

Make-or-Buy Decisions

A common decision for companies is whether to produce a product or service in-house or to outsource it to an external supplier. This decision is based on a comparison of the costs and benefits of both options, including factors such as quality, control, strategic importance, and flexibility. Especially when outsourcing administrative costs, this can transform fixed costs into variable costs.

Problem Identification

Before collecting information, companies need to identify the problem they are trying to solve. This could be anything from reducing costs, increasing sales, improving customer satisfaction, or launching a new product.

- Planning Objects: The specific areas or activities that the company is focusing on for decision-making. Product/production or service; processes; in-house vs. external; determining lower price limits and list prices.

- Planning Horizon: The time frame for which the decision information is relevant. Operative decisions up to one year, depending on the planning object.

- Planning Objectives: The specific goals or outcomes that the company wants to achieve with the decision. Often multidimensional, including both monetary and qualitative criteria (i.e. maximizing operating result while maintaining quality standards).

- Planning Restrictions: The constraints or limitations that the company faces in making the decision. These could include budget constraints, resource limitations, etc. Split into single-product restrictions (upper/lower limit for one decision variable) and multi-product restrictions (limits on several variables, multiple output goods claim a scarce resource).

Information Collection

Quantitative and Qualitative Information

- Quantitative Information: Numerical data that can be measured and analyzed statistically. Examples include daily monetary rates or employee work load.

- Qualitative Information: Non-numerical data that provides insights into opinions, motivations, and behaviors. Examples include customer feedback or employee satisfaction.

Accounting systems provide quantitative information about costs, revenues, and profits, while market research and customer feedback provide qualitative information about customer preferences and satisfaction. Both types of information are crucial for making informed decisions.

Only considering accounting information might ignore positive or negative synergies between products, and can often only approximate a decision’s consequences. However, more qualitative information commonly comes with higher uncertainty and is more difficult to quantify, which can make it harder to use for decision-making.

In some cases, decision-supporting information can be the application of simple decision rules based on a fixed threshold on a quantitative variable.

Requirements for Information

Information collected for decision-making should be:

- Relevant: Directly related to the decision at hand and helps in evaluating alternatives

- Accurate: Free from errors and reliable for making decisions

- Up-to-date: Reflecting the most current data and information available

Relevant Costs

Sunk costs are not relevant (those that have been irrevocably set by past decisions). Opportunity costs (the lost advantage of alternatives) are relevant.

Variable, Absorption, Standard Costing

When decision-making, variable costing tends to be more relevant than absorption costing, as fixed costs often don’t change with the decision and can be considered sunk costs. If fixed costs do change, however, they should be included in the decision-making process.

Standard costing (from the IndustryWeek article) assigns predetermined target costs to products. While useful for budget control and variance analysis, relying on its fixed overhead allocations for make-or-buy decisions can distort true marginal costs and trigger a manufacturing “death spiral.”

Forecasting: Dealing With Uncertainty

The consequences of decisions are generally in the future and therefore uncertain, e.g. with varying demand or fluctuating prices. To deal with this, companies identify different scenarios and determine revenues and costs for each scenario. They can then calculate the expected value of each scenario, which is the probability-weighted average of the outcomes. This allows them to make decisions based on the expected value, rather than just the most likely outcome.

Common Decisions

Product Mix

Deciding which products to produce in which quantities is the most relevant decision of any company. The product mix decision is influenced by factors such as market demand, production capacity, and profitability.

- Without binding multi-product constraints, the relevant decision criterion is the contribution margin of the individual product.

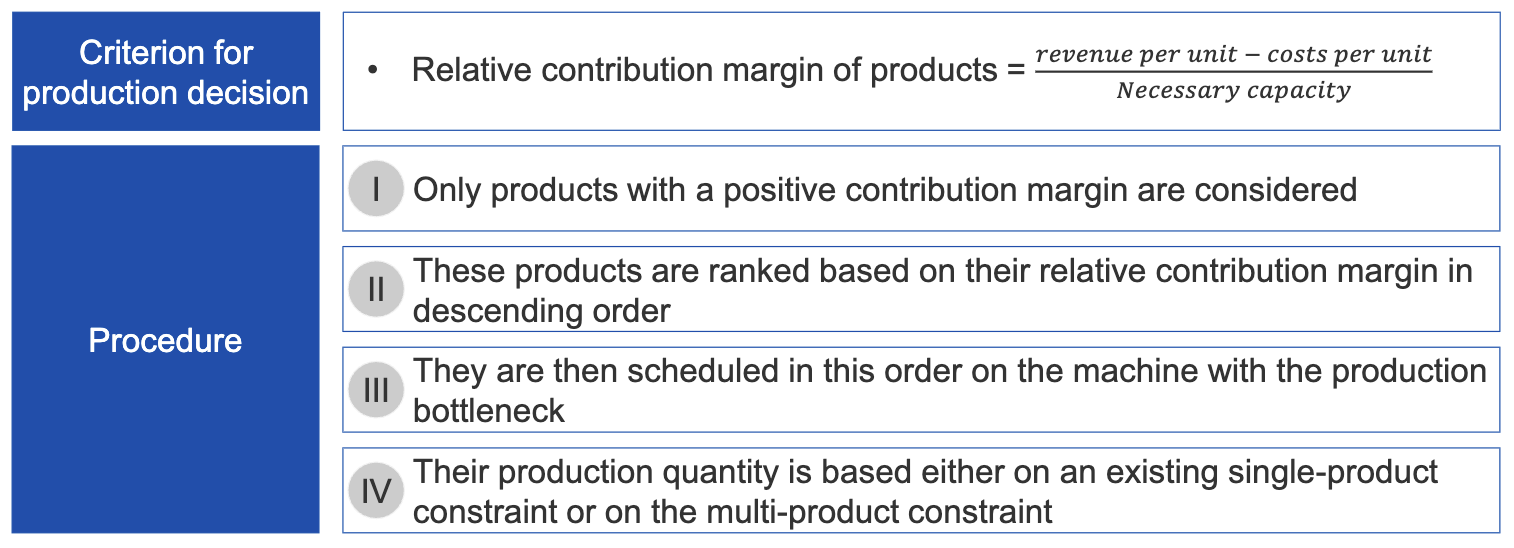

- When there is one binding multi-product constraint, the relevant decision criterion is the relative contribution margin of products.

- When there are multiple multi-product constraints, the relevant decision criterion is the total contribution margin.

The contribution margin is simply:

However, even if a product has a negative contribution margin, it may still make sense to produce due to synergies with other products.

Once the contribution margins are known, the product mix can simply be determined using a linear optimization model, solved using Simplex. Only products with a positive contribution margin are considered (synergies cannot be taken into account here). The optimization maximizes the total contribution margin, subject to the constraints of production capacity and market demand.

Pricing

In terms of pricing, there are two types of companies:

- Price Setters: Can influence the the selling prices of their products; usually industries with few competitors or with customer-specific orders and strong market power.

- Price Takers: Have only a limited influence on price; usually industries with many competitors or with standardized products and weak market power.

For both price takers and setters, a price is determined that matches supply and demand using one of the following approaches:

- Economic Prices: Marginal Revenues equal Marginal Costs, which is the profit-maximizing price. This is explained in Profit Maximum.

- Simplified Pricing: Price equals total costs plus a markup, which is easier to calculate but may not maximize profit.

Lower Price Limit

The lower price limit represents the minimum price required to justify accepting an order or selling a product without worsening the company’s operating result. Its calculation depends on the time horizon and capacity constraints:

- Short-term (Idle Capacity): Equal to the variable costs of the product, as any price above this contributes to covering fixed costs.

- Short-term (Bottleneck): Equal to the variable costs plus opportunity costs (the foregone contribution margin of the next-best product that must be abandoned).

- Long-term: Equal to the total costs (full absorption costs), as all fixed costs become variable and must be covered to sustain operations in the long run.

Long-Term Pricing Decisions

In the long term, companies define an average target price for several months or longer.

This additionally takes into account long-term effects of prices on demand, customers’ willingness to pay, and the company’s ability to adjust capacity.

In contrast to short-term pricing, this also considers fixed costs of capacity; decisions use absorption costing.